Talk in the French wind sector is dominated by the future of Alstom.

And yet, while this talk continues, moves are afoot to attract fresh investment into French onshore wind. An interesting situation, since France has an 8GW install base and is not an obvious candidate for what amounts to an industry kick-start.

This week, French energy minister Segolene Royal announced that new feed-in tariffs for the sector would be revealed imminently.

This follows the cancellation on Wednesday of a long-disputed decree about previous tariffs, which the European Union’s Court of Justice ruled was invalid in December because France had not followed EU state aid rules. Uncertainty over tariffs is one factor that has stifled investment in new wind farms since 2011.

Royal said that the new tariff rules would “end a long period of uncertainty that has destabilised the sector”. It is positive, but the end of investor uncertainty? Really?

The fundamentals for investors in France look good. The left-leaning government is trying to shift the country’s energy mix away from nuclear power, and it sees renewables including wind as the way to do this. Sounds good so far.

The country also has big plans to build on that 8GW. It wants 19GW of onshore wind by 2020, with 6GW offshore. It has to get motoring if it wants to achieve this, because it often takes between six and eight years to get a wind farm from first plans to energy production.

The government wants to remove blockages that stifle development. It adopted new measures in its Brottes law in 2013 to simplify the rules about wind projects, including the scrapping of locally-decided ‘development areas of wind energy’.

In theory, moves like this should help to promote investment. It is likely that it will start to reverse falling numbers of installations, which have dropped year-on-year for four years. Still, we won’t get too excited about what it means for the market’s long-term prospects.

Yes, it is good that the French government is seeking to remove blockages. However, for as long as the French government continues to tinker with the legislative framework, chopping and changing its policies as it reduces reliance on nuclear, uncertainty remains.

Moreover, the French government has been very hands on with General Electric’s bid for Alstom. It has not wanted vital French assets to fall into US hands, and it has been courting German giant Siemens for a rival bid.

This is the kind of behaviour that worries investors. And it underscores a long standing truth that energy remains wholly political.

That said, we’ve already seen good levels of deal flow in the secondary market, especially when schemes have secured consent or are already operational.

Velocita for instance, is building out a portfolio of 23 development projects totalling 750MW that it bought from E.On in May 2011; and Iberdrola offloaded a portfolio of 32 completed onshore projects to a group comprising EDF, General Electric and Munich Re. This proves that the French model can and does work for investors, when the certainty is secured.

The difficulty at the moment is getting projects to that stage of certainty.

Article search

Wind Watch

US and European sanctions against Russia over its invasion of the Crimea clearly make the prospect of investing in Russia look, at best, uncertain.

Does this mean investors will miss the chance to invest in a wind power boom? Not likely. The prospect of a boom is remote, even though Russia is making progress on renewables.

This progress is represented through its new subsidies regime.

The Russian government announced in September a list of 39 projects that would benefit from renewable energy subsidies, including wind farms. This was significant as it was the first ever state support given to renewable energy projects in Russia. And, this month, the government will follow this by revealing more projects that will benefit from the regime.

But to date, wind has not been a big beneficiary. Thirty-two of the 39 projects given backing were solar plants. There were wind projects totalling 1.1GW up for consideration in the first tender round, but only 110MW of them were actually awarded subsidies.

In part, this is because solar power can more easily address the stipulation that the winning schemes have to be able to use at least 50% of locally-produced components.

Clearly, this is a problem for wind. If you don’t have a wind power industry in Russia then how can you source more than 50% of components locally?

Then there’s the practical problem of gaining parts from European or US firms, although it does not close the door to Asia.

Organisations such as the International Finance Corporation have urged Russia to ease local content requirements for wind projects, but to date there is little prospect of this.

As it stands, there are wind farms totalling 1.6GW up for consideration in the second tender, but based on the round one experience, the true figure is likely to be much less.

It is also difficult to believe Russia is serious about wind. It has a target of 3.6GW of wind power by 2020, which is tiny when you compare it to the 91GW already installed in China.

And the nation’s target of 2.5% of energy from renewable sources by 2020 is tiny too. The country currently generates just 0.8% of its energy from renewable sources; and that 2.5% is a reduction on the 4.5% the government had previously agreed in 2009.

It would represent major progress for the country, but also symbolises a weakening of its long-term ambitions.

And there’s another thing. Only last month Russia’s Gazprom and the China National Petroleum Corporation signed a 30-year gas export deal worth an estimated $400bn. It starts in 2018.

The deal was a priority for Russia in the face of increasing energy sanctions from Europe.

Moreover, as the world’s largest natural gas producer, it’s easy to see why renewables including wind, barely features in its thoughts.

Many will be watching the latest tender progress with interest but to suggest that this marks any real shift in Russian energy policy would be far fetched.

For now at least, Russian wind energy remains left out in the cold.

US and European sanctions against Russia over its invasion of the Crimea clearly make the prospect of investing in Russia look, at best, uncertain.

Does this mean investors will miss the chance to invest in a wind power boom? Not likely. The prospect of a boom is remote, even though Russia is making progress on renewables.

This progress is represented through its new subsidies regime.

The Russian government announced in September a list of 39 projects that would benefit from renewable energy subsidies, including wind farms. This was significant as it was the first ever state support given to renewable energy projects in Russia. And, this month, the government will follow this by revealing more projects that will benefit from the regime.

But to date, wind has not been a big beneficiary. Thirty-two of the 39 projects given backing were solar plants. There were wind projects totalling 1.1GW up for consideration in the first tender round, but only 110MW of them were actually awarded subsidies.

In part, this is because solar power can more easily address the stipulation that the winning schemes have to be able to use at least 50% of locally-produced components.

Clearly, this is a problem for wind. If you don’t have a wind power industry in Russia then how can you source more than 50% of components locally?

Then there’s the practical problem of gaining parts from European or US firms, although it does not close the door to Asia.

Organisations such as the International Finance Corporation have urged Russia to ease local content requirements for wind projects, but to date there is little prospect of this.

As it stands, there are wind farms totalling 1.6GW up for consideration in the second tender, but based on the round one experience, the true figure is likely to be much less.

It is also difficult to believe Russia is serious about wind. It has a target of 3.6GW of wind power by 2020, which is tiny when you compare it to the 91GW already installed in China.

And the nation’s target of 2.5% of energy from renewable sources by 2020 is tiny too. The country currently generates just 0.8% of its energy from renewable sources; and that 2.5% is a reduction on the 4.5% the government had previously agreed in 2009.

It would represent major progress for the country, but also symbolises a weakening of its long-term ambitions.

And there’s another thing. Only last month Russia’s Gazprom and the China National Petroleum Corporation signed a 30-year gas export deal worth an estimated $400bn. It starts in 2018.

The deal was a priority for Russia in the face of increasing energy sanctions from Europe.

Moreover, as the world’s largest natural gas producer, it’s easy to see why renewables including wind, barely features in its thoughts.

Many will be watching the latest tender progress with interest but to suggest that this marks any real shift in Russian energy policy would be far fetched.

For now at least, Russian wind energy remains left out in the cold.

Siemens to axe wind from Alstom offer

Siemens is poised to make a formal bid for Alstom’s energy assets but without including wind, nuclear or transmission in its offer.

The German manufacturer entered the race for the assets last month in a bid to scupper a deal proposed by US giant General Electric. The French government has courted Siemens as it does not want to see vital assets fall into US hands.

Siemens is set to propose a transfer of its rail activities and around €7bn in cash in exchange for some of Alstom’s energy assets. Keeping wind and nuclear out of the bid would enable Alstom to sell them to state-owned French firm Areva.

Enercon enters energy trading market

Enercon will next month enter the energy trading market to enable wind farm operators to trade their electricity on the wholesale market.

The German manufacturer has said it will work with more than 30 electricity trading firms to offer the service to German wind farms. Enercon will remotely control the operation of turbines and supply this energy directly to customers.

Germany's revised Renewable Energy Act legislates that, from August, all electricity commissioned from turbines after then must be marketed on the wholesale market.

Unesco warns UK over Navitus Bay

Unesco has warned that the 95-mile Jurassic Coast in southern England could lose its world heritage site status if the £3.5bn Navitus Bay project is built.

The organisation, part of the United Nations, has written to the UK Government to say that the 970MW 194-turbine offshore scheme would have a negative impact on views between Dorset and the Isle of Wight. The Jurassic Coast comprises 96 miles in Dorset and East Devon, and is England’s only natural heritage site.

Eneco and EDF Energy submitted their planning application for the scheme last month. The developers said the scheme would not have a significant impact on the protected views, and are seeking clarification from the UK Government.

Vestas names central European president

Vestas has named Christoph Vogel as its new president of in central Europe and group senior vice president.

Vogel joins the Danish manufacturer from Johnson Controls, where he is vice president and general manager of the global workplace solutions and life sciences divisions. He will officially take up the post on 1 June.

Vogel has previously worked for Siemens and The Boston Consulting Group.

EDP: "Onshore wind cheaper than coal"

Onshore wind is the cheapest form of utility-scale onshore energy generation in Europe, according to research by EDP Renovaveis.

The Spanish utility has reported the levelled cost of electricity from onshore wind in Europe is one-third cheaper than coal and 20% cheaper than gas. The finding is significant because the firm has wind, fossil fuels and hydropower assets.

EDP Renovaveis also said that wind is cheaper than traditional power sources in countries including the US, Brazil, Mexico, South Africa and major markets in Asia.

Wind Watch

It is easy to blame the media when things don’t work out.

The rise of extremist political parties, panic over pandemics and other things we don’t like. Yet this ignores the real reasons these things happen.

The tendency to point the finger at the media when things go wrong is why it is easy to be cynical about the statement from Temporis Capital regarding challenges experienced during a recent fundraising.

If you haven’t read it, Temporis claimed that negative coverage of wind farms in the UK may have harmed a recent clean energy fundraising. The firm was looking to raise £20m for its existing Ventus VTS Plc (VEN) and Ventus 2 VCT Plc trusts, to invest in UK wind and hydro schemes. In the event, it raised £4m.

But it seems unlikely that negative press reports directly contributed to this.

The more conservative parts of the UK media have long been hostile to wind farms, just as they have been in North America and Australia. This hasn’t got any worse recently, and there is no reason to believe a fundraising now would be more impacted now than in 2013.

What has changed in the UK over the last couple of months is that the Conservative Party has stepped up its anti-wind-farm rhetoric. Communities secretary Eric Pickles extended the period during which he has final say over new wind farms to the 2015 general election; and after that, the Conservatives have mooted a ban on all new onshore wind farms.

The media reported these stories, but it is the government’s attitude to wind farms that is more likely to affect investors. And it is right that investors know about this.

So let’s set aside the point about the media and look at other possible reasons that investors might have passed up on the opportunity to invest with Temporis.

First, it is worth noting that the fund plans to invest in wind and hydro projects, yet many investors remain unconvinced on the precise workings and profitability of hydro. It’s natural for people to avoid deals they don’t understand, particularly with new technology.

Second, Temporis was looking to raise a relatively small amount of money. It may seem counterintuitive but, as history shows, it is often more difficult to raise smaller pools of capital, since the demographics of the investor base are markedly different and the individual pay-off often significantly reduced.

Remember, as the fund raising by John Laing Environmental Assets has shown this year, there’s no shortage of capital. It raised £160m, against an aim of £170m.

And perhaps we also have to look at the way in which the opportunity was communicated and sold. This element of fund management has become critical.

Get it right and investor clarity and confidence grows. Get it wrong and the fund only ever serves to muddy the waters. The communications made timed tocoincide with the 2014 Budget having been a case in point.

Naturally, there may well be other reasons at play here – and of course, it’s painfully easy to sit on the sidelines and proffer comment.

Nevertheless, with fresh capital having been poured into an increasingly diverse pool of listed renewable energy opportunities, the need for funds to work hard to engage and interact with prospective investors is becoming increasingly apparent.

It is easy to blame the media when things don’t work out.

The rise of extremist political parties, panic over pandemics and other things we don’t like. Yet this ignores the real reasons these things happen.

The tendency to point the finger at the media when things go wrong is why it is easy to be cynical about the statement from Temporis Capital regarding challenges experienced during a recent fundraising.

If you haven’t read it, Temporis claimed that negative coverage of wind farms in the UK may have harmed a recent clean energy fundraising. The firm was looking to raise £20m for its existing Ventus VTS Plc (VEN) and Ventus 2 VCT Plc trusts, to invest in UK wind and hydro schemes. In the event, it raised £4m.

But it seems unlikely that negative press reports directly contributed to this.

The more conservative parts of the UK media have long been hostile to wind farms, just as they have been in North America and Australia. This hasn’t got any worse recently, and there is no reason to believe a fundraising now would be more impacted now than in 2013.

What has changed in the UK over the last couple of months is that the Conservative Party has stepped up its anti-wind-farm rhetoric. Communities secretary Eric Pickles extended the period during which he has final say over new wind farms to the 2015 general election; and after that, the Conservatives have mooted a ban on all new onshore wind farms.

The media reported these stories, but it is the government’s attitude to wind farms that is more likely to affect investors. And it is right that investors know about this.

So let’s set aside the point about the media and look at other possible reasons that investors might have passed up on the opportunity to invest with Temporis.

First, it is worth noting that the fund plans to invest in wind and hydro projects, yet many investors remain unconvinced on the precise workings and profitability of hydro. It’s natural for people to avoid deals they don’t understand, particularly with new technology.

Second, Temporis was looking to raise a relatively small amount of money. It may seem counterintuitive but, as history shows, it is often more difficult to raise smaller pools of capital, since the demographics of the investor base are markedly different and the individual pay-off often significantly reduced.

Remember, as the fund raising by John Laing Environmental Assets has shown this year, there’s no shortage of capital. It raised £160m, against an aim of £170m.

And perhaps we also have to look at the way in which the opportunity was communicated and sold. This element of fund management has become critical.

Get it right and investor clarity and confidence grows. Get it wrong and the fund only ever serves to muddy the waters. The communications made timed tocoincide with the 2014 Budget having been a case in point.

Naturally, there may well be other reasons at play here – and of course, it’s painfully easy to sit on the sidelines and proffer comment.

Nevertheless, with fresh capital having been poured into an increasingly diverse pool of listed renewable energy opportunities, the need for funds to work hard to engage and interact with prospective investors is becoming increasingly apparent.

Developers are an entrepreneurial bunch. The best of them are calculating risk-takers that break away from the mainstream in hunt of big ticket deals.

This makes the announcement by the UK’s Crown Estate earlier this week look curious. The UK-based property business is on the lookout for a developer to take on the task of bringing the Blyth Offshore Wind Demonstrator project online by 2017. The site received planning consent for a 99MW scheme last November.

In theory, this announcement should fire the starting gun for developers to start sharpening their pencils and submitting their project tenders and bids.

After all, the best sites rarely get an airing like this. They’re snapped up far earlier in the development cycle when there is far less fanfare or active marketing.

So what’s different here? Why is this project being so actively marketed?

Perhaps this is because initial interest behind the scenes has been muted, at best. It is clear that developers have not been quick to take this site off the market.

This lethargy from developers may be due to the proposed locations of turbines. Only five of the sites are in shallow seas and the majority in far deeper waters. The nature of the site makes it a more difficult prospect to develop than usual.

There is also the desire for developers to use Blyth to test new of turbines and other kit, in keeping with the site’s proposed use for testing and development. That alone requires some deft management of internal stakeholders, quite apart from the complexities it adds to future cabling connections and the grid.

However, perhaps the most interesting element is what this lack of interest thus far tells us about the difference between the opportunity on offer and developer ambitions. For developers, their ambitions are focused on revenue generation and a move towards greater profitability. This means focusing on project that can be developed and rolled out at scale, rather than speculative research projects.

Only by focusing on replicable schemes can developers maximise margins, build out the supply chain, and provide a commercially-focused platform through which to introduce new technologies and drive down industry costs.

Demonstrator sites have already played an important role in the early-stage development in the industry, and few people question their past value.

But, by their very nature, demonstrator schemes are also difficult to handle, come with added complexities, and require significant hands-on support. Many developers have already privately acknowledged that this makes the Blyth initiative and interesting but challenging proposition.

While providing on-site contractor support could be compelling, it takes far more operational and financial commitment to take on the overall development risk.

That’s not to say a developer won’t be found — we think one will. Just don't be surprised if we see new market entrants, perhaps even from Asia, take a look.

Wind Watch

Developers are an entrepreneurial bunch. The best of them are calculating risk-takers that break away from the mainstream in hunt of big ticket deals.

This makes the announcement by the UK’s Crown Estate earlier this week look curious. The UK-based property business is on the lookout for a developer to take on the task of bringing the Blyth Offshore Wind Demonstrator project online by 2017. The site received planning consent for a 99MW scheme last November.

In theory, this announcement should fire the starting gun for developers to start sharpening their pencils and submitting their project tenders and bids.

After all, the best sites rarely get an airing like this. They’re snapped up far earlier in the development cycle when there is far less fanfare or active marketing.

So what’s different here? Why is this project being so actively marketed?

Perhaps this is because initial interest behind the scenes has been muted, at best. It is clear that developers have not been quick to take this site off the market.

This lethargy from developers may be due to the proposed locations of turbines. Only five of the sites are in shallow seas and the majority in far deeper waters. The nature of the site makes it a more difficult prospect to develop than usual.

There is also the desire for developers to use Blyth to test new of turbines and other kit, in keeping with the site’s proposed use for testing and development. That alone requires some deft management of internal stakeholders, quite apart from the complexities it adds to future cabling connections and the grid.

However, perhaps the most interesting element is what this lack of interest thus far tells us about the difference between the opportunity on offer and developer ambitions. For developers, their ambitions are focused on revenue generation and a move towards greater profitability. This means focusing on project that can be developed and rolled out at scale, rather than speculative research projects.

Only by focusing on replicable schemes can developers maximise margins, build out the supply chain, and provide a commercially-focused platform through which to introduce new technologies and drive down industry costs.

Demonstrator sites have already played an important role in the early-stage development in the industry, and few people question their past value.

But, by their very nature, demonstrator schemes are also difficult to handle, come with added complexities, and require significant hands-on support. Many developers have already privately acknowledged that this makes the Blyth initiative and interesting but challenging proposition.

While providing on-site contractor support could be compelling, it takes far more operational and financial commitment to take on the overall development risk.

That’s not to say a developer won’t be found — we think one will. Just don't be surprised if we see new market entrants, perhaps even from Asia, take a look.

Crown hunts Narec replacement at Blyth

The Crown Estate has started the hunt for a development partner for the 99MW Blyth offshore wind demonstration project.

The Crown Estate was due to partner with the National Renewable Energy Centre (Narec) on the site, and Narec had been seeking partners at the 15-turbine site. However, Narec merged with the Offshore Renewable Energy Catapult last month.

The 14km site won consent in November for largest offshore wind demonstration project in the UK. It is planned a location where developers can deploy innovative technology in deeper waters than usual; and scheduled to be operational by 2017.

Areva ponders deal for Alstom assets

Areva would be interested in considering a deal for Alstom’s wind turbines unit as part of General Electric’s proposed takeover of Alstom’s energy arm.

Luc Oursel, chief executive of Areva, told a French parliamentary hearing about nuclear energy that it would be willing to examine possibilities. However, he added that the French manufacturer was not currently in talks about a deal for the unit.

The government has been hostile to GE’s planned takeover of Alstom’s energy assets, and the sale of Alstom’s turbine activities to a French investor is one option to make the deal more palatable.

138MW South Africa project begins operations

The 138MW Jeffreys Bay scheme on South Africa’s Eastern Cape has started exporting power to South African utility Eskom.

Developer Jeffreys Bay Wind Farm, which is a consortium that includes Globeleq and Mainstream Renewable Power, said the 60-turbine scheme is due to begin commercial operations later this month.

The development is one of the first wind farms being developed by the South African Government’s Renewable Energy Independent Power Producer Procurement Programme; and is one of the largest wind farms in South Africa. It has a 20-year power purchase agreement with Eskom.

MHI Vestas considers Hull for UK factory

MHI Vestas is reportedly considering opening a new offshore wind factory in Hull as it seeks locations in the UK.

The company, a joint venture between Japanese giant Mitsubishi Heavy Industries and Danish manufacturer Vestas, was officially formed on 1 April. The Hull Daily Mail said MHI Vestas is looking at a site in East Riding to build a factory employing up to 500 people. This would be close to a factory being developed by Siemens.

A spokesman from MHI Vestas said the company was keen to move to the UK and was exploring its options, but would not comment on Hull specifically.

WPD legal action over 1GW French tender

German developer WPD has launched a legal challenge against the French government’s award of a €4bn offshore tender to a consortium led by GDF Suez.

On 7 May, the government awarded the GDF-led group the right to develop two projects totalling 1GW. WPD was part of a rival consortium with French utility EDF and Alstom. The German firm is challenging the tender award for the 500MW project near the islands of Noirmoutier and Yeu, off the west coast.

WPD said the GDF-led group has chosen a foundation that was not compatible with soil at the site; and it wants a judge to investigate why energy regulator CRE recommended the GDF bid.

Wind Watch

The use of canaries in British coal mines came to an end in 1987. However, in the 27 years since, the industry hasn't gone the way of the poor songbird. It's boomed.

Countries talk a good game about embracing green energy, including wind. Many are doing so. But the ‘black stuff’ still provides 40% of global electricity needs.

Look at the world’s biggest wind markets.

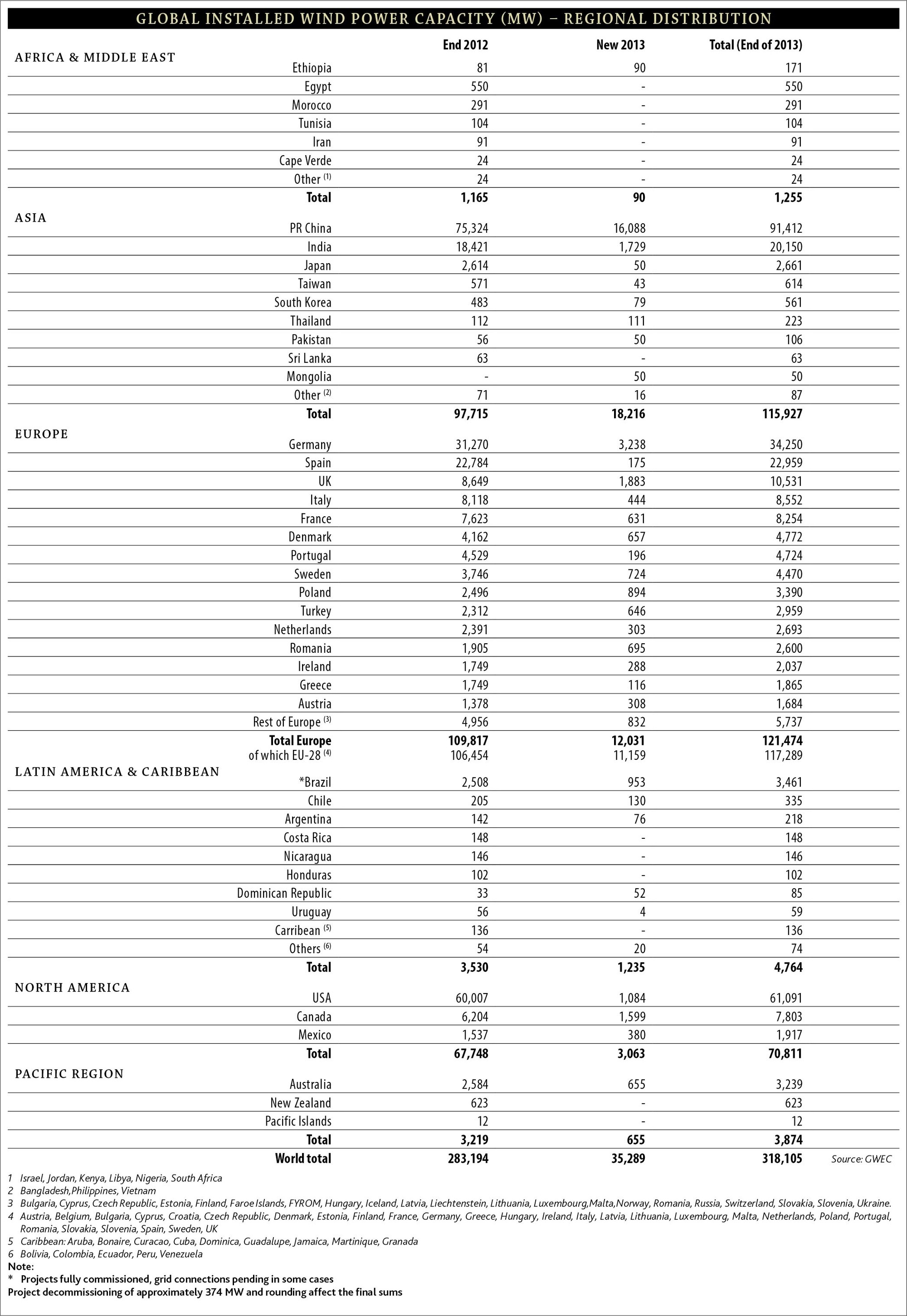

China has most installed wind power (91GW), but it is also the world’s largest coal producer and consumer. The US has the second most installed wind power (61GW), but it is also the world’s second-largest producer of coal.

Meanwhile, the International Energy Agency has said annual coal consumption grew 60% between 2000 and 2012; and it has forecast that demand will grow on average 2.3% a year until 2018. Coal prices have fallen due to oversupply and weaker-than-expected demand, but this has simply forced producers to cut their costs in order to maximise profits.

The only possible bright spot is that growth in demand is slowing. But we see little evidence that either appetite for coal or confidence in the sector is dwindling.

This brings us to the disaster in Soma in Turkey.

This accident is awful. It has killed 301 coal miners, and again highlights how dirty and dangerous the coal industry is compared to most energy sources.

But it is only the size of this one accident that is unprecedented. Deaths in the coal sector are commonplace. More than 1,000 workers died in Chinese coal mines last year, and 50 in the US. And that’s before you factor in long-term health issues.

Even so, disasters like Soma are increasing pressure from utilities on energy producers to source their coal from more ethical sources. And that pressure is coming from all angles. At one extreme it includes the Norwegian sovereign wealth fund and, at the other, the Pope.

Unsurprisingly then, this pressure has started to have some effect. For example, in 2012, a group of major coal buyers formed the Bettercoal initiative to improve ethical standards.

But here’s the thing. Despite these changes, there is no a big global move away from coal. The US may burn less of the stuff but they still willingly sell it – it remains a significant all-American export.

Worse still, even if global sales do start to dry up, it won’t necessarily lead to a big move towards wind. It could equally benefit shale gas, nuclear and oil.

However, it’s not time for the wind industry to lose heart. Rather, it’s a timely reminder that as an industry we must continue to innovate, invest and evolve. That means focusing on the introduction of more efficient turbines and on technology that can make its contributions to the grid less intermittent.

It also means we must avoid the temptation to point towards the disaster in Turkey and focus solely on how it demonstrates coal’s shortcomings. Focusing on wind's positive commercial impacts is a much more tuneful song to sing.

{kind=link}

The use of canaries in British coal mines came to an end in 1987. However, in the 27 years since, the industry hasn't gone the way of the poor songbird. It's boomed.

Countries talk a good game about embracing green energy, including wind. Many are doing so. But the ‘black stuff’ still provides 40% of global electricity needs.

Look at the world’s biggest wind markets.

China has most installed wind power (91GW), but it is also the world’s largest coal producer and consumer. The US has the second most installed wind power (61GW), but it is also the world’s second-largest producer of coal.

Meanwhile, the International Energy Agency has said annual coal consumption grew 60% between 2000 and 2012; and it has forecast that demand will grow on average 2.3% a year until 2018. Coal prices have fallen due to oversupply and weaker-than-expected demand, but this has simply forced producers to cut their costs in order to maximise profits.

The only possible bright spot is that growth in demand is slowing. But we see little evidence that either appetite for coal or confidence in the sector is dwindling.

This brings us to the disaster in Soma in Turkey.

This accident is awful. It has killed 301 coal miners, and again highlights how dirty and dangerous the coal industry is compared to most energy sources.

But it is only the size of this one accident that is unprecedented. Deaths in the coal sector are commonplace. More than 1,000 workers died in Chinese coal mines last year, and 50 in the US. And that’s before you factor in long-term health issues.

Even so, disasters like Soma are increasing pressure from utilities on energy producers to source their coal from more ethical sources. And that pressure is coming from all angles. At one extreme it includes the Norwegian sovereign wealth fund and, at the other, the Pope.

Unsurprisingly then, this pressure has started to have some effect. For example, in 2012, a group of major coal buyers formed the Bettercoal initiative to improve ethical standards.

But here’s the thing. Despite these changes, there is no a big global move away from coal. The US may burn less of the stuff but they still willingly sell it – it remains a significant all-American export.

Worse still, even if global sales do start to dry up, it won’t necessarily lead to a big move towards wind. It could equally benefit shale gas, nuclear and oil.

However, it’s not time for the wind industry to lose heart. Rather, it’s a timely reminder that as an industry we must continue to innovate, invest and evolve. That means focusing on the introduction of more efficient turbines and on technology that can make its contributions to the grid less intermittent.

It also means we must avoid the temptation to point towards the disaster in Turkey and focus solely on how it demonstrates coal’s shortcomings. Focusing on wind's positive commercial impacts is a much more tuneful song to sing.

It is easy to dismiss the French government as being needlessly hostile and over-emotional to GE’s bid for Alstom’s energy arm.

However, it isn’t alone in fighting for its national assets.

This week, UK MPs grilled Pfizer chief executive officer Ian Read over the US pharma giant’s proposed £63bn takeover of troubled drug maker AstraZeneca. Read told a House of Commons select committee that the proposed takeover would speed up development of Astra’s drugs; but critics of the deal warned that Pfizer would slash both jobs and R&D spending.

Both governments want to protect their “crown jewels” against vicious cuts. That is a natural instinct in any planned takeover, and we expect similar debates to rage in boardrooms in the wind sector in the coming years as consolidation takes hold.

The GE-Alstom proposal is the highest-profile example to date of takeover activity, but joint ventures such as Vestas-Mitsubishi and Areva-Gamesa demonstrate a growing appeal for corporate tie-ups.

However, regardless of what the government thinks, the ultimate decision over whether to proceed with a takeover surely rests with the senior corporate board.

In theory at least, they are the people with the best understanding of what is in the interests of the company and its shareholders. This is as true in wind as any other part of the economy.

Governments are right to grill companies over proposed takeovers and argue the case for the protection of jobs and national interests. They are right to push for cast-iron company commitments, too.

But, in a free market, the final decision about what is right for the potential acquiree must rest with that firm’s management.

It is not the government’s place to introduce takeover laws to stop the deal from happening, although this is what the French government has done this week with a decree that allows it to block foreign takeovers of “strategic” companies.

This has also been mooted in the UK, but t would be a dangerous step.

Yes, the UK government could use protectionist laws to stop the takeover of AstraZeneca, and that might protect some UK jobs today. But it ignores the jobs that would never be created in the UK if firms see it as a bad place to do business.

And that’s not the only thing. When it comes to acquisitions and mergers, there’s rarely an option that's 100% right or 100% wrong. Sure, we might not like the final result but how can we guarantee that the alternative would have been any better?

This is the challenge facing Alstom as it maps out the plans for its future.

It is also one of the perils of operating in a free market economy. Some takeovers will provide the rocket fuel needed for future market success, while others may end in job losses, asset stripping and steady demise.

Clearly, nobody wants the latter, but sentimentality from politicians and corporate leaders does not necessarily result in the best option. As the wind industry goes global, it is important to remember the limitations of corporate sentimentality.

Wind Watch

It is easy to dismiss the French government as being needlessly hostile and over-emotional to GE’s bid for Alstom’s energy arm.

However, it isn’t alone in fighting for its national assets.

This week, UK MPs grilled Pfizer chief executive officer Ian Read over the US pharma giant’s proposed £63bn takeover of troubled drug maker AstraZeneca. Read told a House of Commons select committee that the proposed takeover would speed up development of Astra’s drugs; but critics of the deal warned that Pfizer would slash both jobs and R&D spending.

Both governments want to protect their “crown jewels” against vicious cuts. That is a natural instinct in any planned takeover, and we expect similar debates to rage in boardrooms in the wind sector in the coming years as consolidation takes hold.

The GE-Alstom proposal is the highest-profile example to date of takeover activity, but joint ventures such as Vestas-Mitsubishi and Areva-Gamesa demonstrate a growing appeal for corporate tie-ups.

However, regardless of what the government thinks, the ultimate decision over whether to proceed with a takeover surely rests with the senior corporate board.

In theory at least, they are the people with the best understanding of what is in the interests of the company and its shareholders. This is as true in wind as any other part of the economy.

Governments are right to grill companies over proposed takeovers and argue the case for the protection of jobs and national interests. They are right to push for cast-iron company commitments, too.

But, in a free market, the final decision about what is right for the potential acquiree must rest with that firm’s management.

It is not the government’s place to introduce takeover laws to stop the deal from happening, although this is what the French government has done this week with a decree that allows it to block foreign takeovers of “strategic” companies.

This has also been mooted in the UK, but t would be a dangerous step.

Yes, the UK government could use protectionist laws to stop the takeover of AstraZeneca, and that might protect some UK jobs today. But it ignores the jobs that would never be created in the UK if firms see it as a bad place to do business.

And that’s not the only thing. When it comes to acquisitions and mergers, there’s rarely an option that's 100% right or 100% wrong. Sure, we might not like the final result but how can we guarantee that the alternative would have been any better?

This is the challenge facing Alstom as it maps out the plans for its future.

It is also one of the perils of operating in a free market economy. Some takeovers will provide the rocket fuel needed for future market success, while others may end in job losses, asset stripping and steady demise.

Clearly, nobody wants the latter, but sentimentality from politicians and corporate leaders does not necessarily result in the best option. As the wind industry goes global, it is important to remember the limitations of corporate sentimentality.

E.On calls for green energy compensation

E.On has called for compensation for losses incurred at gas-fired power stations due to the expansion of renewable energy in Germany, including wind farms.

The German utility made the call as it revealed a 12% drop in first-quarter earnings year-on-year. It said a growing proportion of renewable energy in the German grid is making it tough to run conventional power stations profitably, and compensation for these power stations was key to maintaining a reliable energy network.

Meanwhile, E.On’s renewables arm saw first-quarter sales fall 8% to €614m; but investments in wind and solar projects doubled to €183m, driven by investments in two offshore projects: 230MW Humber Gateway and 288MW Amrumbank West.

Enel grows stake in 250MW Buffalo Dunes

Enel Green Power has agreed to pay $60m to grow its stake in 250MW US wind farm Buffalo Dunes to 75%.

The Italian utility’s North American unit has signed a deal with GE Capital to buy a further 26% stake in the company that runs the US wind farm. GE Capital will retain at the remaining 25% stake.

This is part of Enel’s strategy, revealed last month, to shift its attention from core markets in Italy and Spain towards emerging markets and North America.

Ireland: “Offshore wind key to energy future”

Developing Ireland's offshore wind sector is vital for energy security and the development of a green energy export market, a government report has said.

On Monday, the Irish government published its draft energy “green paper” about how the country can make the transition to local low-carbon energy generation.

It said growing the offshore energy sector is vital: “Ireland has a sea area around ten times the size of its landmass, with one of the best offshore renewable energy (wind, wave and tidal) resources in the world.”

The paper added that the ocean energy sector could make a major contribution to economic growth and job creation to 2030 and beyond. Consultation on the green paper is now ongoing until 31 July.

EDF completes 150MW scheme in Turkey

EDF Energy has completed the commissioning of a 150MW scheme in the Turkish village Geycek, which was developed by its local subsidiary Polat Enerji.

The French utility owns a 45% stake in the project and a Canadian institutional investor also owns a 45% stake. The remaining 10% is owned by businessman Adnan Polat’s Batiyel group, which has developed eight wind farms in Turkey. Four of these started production in 2013.

The Geycek project takes EDF’s installed capacity in Turkey to more than 500MW.

Ketraco consults DNV on Kenya connection

Kenya Electricity Transmission Company (Ketraco) has appointed DNV GL to advise on the construction of a high-voltage link for the Lake Turkana wind farm.

The energy consultant has advised the the state-owned transmission firm on the technical aspects of developing the 426km overhead line. The 400kV transmission scheme will link the 310MW Lake Turkana into the grid at Suswa, which is 80km northwest of Nairobi.

The link is vital to making Lake Turkana — set to be one of Africa’s biggest wind farms — commercially viable, and improving Kenya’s grid infrastructure.

Wind Watch

In one month, football fans’ eyes will be on Brazil as the World Cup kicks off.

But people will not just be focusing on the opening match between the hosts and Croatia. Talk will also focus on construction delays: three of 12 tournament stadia aren't ready, and some supporting infrastructure is being scaled back or scrapped.

There is a parallel with what has happened in Brazil’s wind sector. The idea of hosting a sizeable wind industry looks exciting, but infrastructure is letting it down.

Brazil has embraced renewables. Hydroelectricity of 86GW makes up two-thirds of the country’s installed energy capacity, and wind accounts for a comparatively tiny 3.5GW. However, the government wants to grow wind to support other sources.

Capacity has been growing fast. For example, when the country was awarded the right to host this year’s World Cup in 2007 it had 247MW of installed capacity. Since then, capacity has grown 14-fold to 3.5GW.

But life has not been a carnival for investors and developers.

Many of these new wind farms are still not linked to the grid because of connection delays by state-run utility Chesf. Earlier this year, there were 48 wind farms without connections, and developers are sceptical that Chesf will meet its revised deadline of the end of this year.

The public is still paying more than $200m a year in government subsidies for the energy produced by these unconnected wind farms.

Politically, this puts the wind sector in a tough position. We need only look to last summer’s riots about the state of public services and the cost of hosting the World Cup and 2016 Olympics to see how incendiary this issue is.

Thankfully for Chesf, the public has bigger concerns than the cost of paying for energy that is not being fed into the grid issue. Nevetheless, its record should make investors question the realism of Brazil’s wind ambitions.

The government now has a target of 17GW of installed capacity by 2020. Some analysts have even forecast that wind power in Brazil could reach 24GW by 2020.

This would present investment opportunities for developers and manufacturers.

But investors will rightly be cautious if transmission problems aren't fixed. Wind is a maturing asset class, and delays and missed deadlines are not good enough.

If there are hundreds of wind farms waiting to be linked to the grid then this would do major damage to the wind industry in Brazil and South America, not to mention individual investment strategies.

The country is also on the cusp of moving into offshore wind, which presents its own transmission problems. Developer Eolica Brasil said this month that it wants to start work in the near future on the first 1GW of its planned 11.2GW Asa Branca offshore project. It is planning a 12MW pilot in 2016 followed by a 258MW demonstrator project in 2017.

Investors will want to see that Brazil is learning from established offshore wind markets in Germany and England — even if it doesn’t copy their style on the pitch.

In one month, football fans’ eyes will be on Brazil as the World Cup kicks off.

But people will not just be focusing on the opening match between the hosts and Croatia. Talk will also focus on construction delays: three of 12 tournament stadia aren't ready, and some supporting infrastructure is being scaled back or scrapped.

There is a parallel with what has happened in Brazil’s wind sector. The idea of hosting a sizeable wind industry looks exciting, but infrastructure is letting it down.

Brazil has embraced renewables. Hydroelectricity of 86GW makes up two-thirds of the country’s installed energy capacity, and wind accounts for a comparatively tiny 3.5GW. However, the government wants to grow wind to support other sources.

Capacity has been growing fast. For example, when the country was awarded the right to host this year’s World Cup in 2007 it had 247MW of installed capacity. Since then, capacity has grown 14-fold to 3.5GW.

But life has not been a carnival for investors and developers.

Many of these new wind farms are still not linked to the grid because of connection delays by state-run utility Chesf. Earlier this year, there were 48 wind farms without connections, and developers are sceptical that Chesf will meet its revised deadline of the end of this year.

The public is still paying more than $200m a year in government subsidies for the energy produced by these unconnected wind farms.

Politically, this puts the wind sector in a tough position. We need only look to last summer’s riots about the state of public services and the cost of hosting the World Cup and 2016 Olympics to see how incendiary this issue is.

Thankfully for Chesf, the public has bigger concerns than the cost of paying for energy that is not being fed into the grid issue. Nevetheless, its record should make investors question the realism of Brazil’s wind ambitions.

The government now has a target of 17GW of installed capacity by 2020. Some analysts have even forecast that wind power in Brazil could reach 24GW by 2020.

This would present investment opportunities for developers and manufacturers.

But investors will rightly be cautious if transmission problems aren't fixed. Wind is a maturing asset class, and delays and missed deadlines are not good enough.

If there are hundreds of wind farms waiting to be linked to the grid then this would do major damage to the wind industry in Brazil and South America, not to mention individual investment strategies.

The country is also on the cusp of moving into offshore wind, which presents its own transmission problems. Developer Eolica Brasil said this month that it wants to start work in the near future on the first 1GW of its planned 11.2GW Asa Branca offshore project. It is planning a 12MW pilot in 2016 followed by a 258MW demonstrator project in 2017.

Investors will want to see that Brazil is learning from established offshore wind markets in Germany and England — even if it doesn’t copy their style on the pitch.

South Africans went to the polls this week in a highly significant set of elections.

These are the first since the death of Nelson Mandela in December, and the first “born free” elections. This means some voters have never lived under apartheid.

The result is also set to have ramifications for those in the country’s wind sector.

The African National Congress (ANC) is expected to win for the fifth time running, although the results are not yet in. But don’t let this fool you into thinking everyone loves the ANC. The party is being dogged by scandals and economic difficulties.

One of its most pressing challenges is to fix the energy system. South Africa is not generating enough energy, and there were rolling blackouts in March when heavy rain made coal supplies too wet to burn at some of its power stations.

This makes it sound like the country should be whole-heartedly embracing renewable energy sources. Alas, it isn’t that simple.

Yes, South Africa’s wind sector is growing. It had just 10MW of wind capacity installed at the start of this year, and the Global Wind Energy Council expects installations of up to 1GW this year. South Africa also has a target of developing 5GW of wind power by 2019.

It is good to see wind finally taking off in South Africa.

But most of its political leaders still see wind as a marginal concern. The ANC is keeping faith with coal despite the blackouts as it wants to exploit the country’s huge reserves. South Africa has the seventh-largest coal reserves in the world and gains more than three-quarters of its primary energy from coal. The ANC wants to make sure it extracts maximum value from this ‘black gold’.

This is why state-owned electricity utility Eskom is building the third- and fourth-largest coal-fired power stations in the southern hemisphere, called Medupi and Kusile, with total capacity of 9.6GW. They are due to start producing power this year, and a third plant of a similar size - Coal 3 - may follow.

Wind may be of little interest to Eskom or leaders with vested interests in the coal sector. But the election should still give hope to wind developers and investors.

We should not forget that the Department of Energy is providing support to the sector with mechanisms like its Renewable Energy Independent Power Producer Procurement Programme (REIPPPP). It is vital for South African wind businesses to demonstrate the value of the first wave of wind farms if support is to continue.

The industry should also be able to benefit from a public backlash where people are demanding a stable energy system by the time of the next elections in 2019. Companies in the wind sector should be able to demonstrate how wind farms can help make the energy network more diverse - and help to keep the lights on.

The ANC will come under major pressure to deliver a more stable and secure energy network. This gives an opportunity for those in the wind sector.

Yes, some prominent ANC backers have vested interests in coal, but ANC leaders also have a vested interest in getting re-elected. Energy security will be vital.[/private/

Wind Watch

South Africans went to the polls this week in a highly significant set of elections.

These are the first since the death of Nelson Mandela in December, and the first “born free” elections. This means some voters have never lived under apartheid.

The result is also set to have ramifications for those in the country’s wind sector.

The African National Congress (ANC) is expected to win for the fifth time running, although the results are not yet in. But don’t let this fool you into thinking everyone loves the ANC. The party is being dogged by scandals and economic difficulties.

One of its most pressing challenges is to fix the energy system. South Africa is not generating enough energy, and there were rolling blackouts in March when heavy rain made coal supplies too wet to burn at some of its power stations.

This makes it sound like the country should be whole-heartedly embracing renewable energy sources. Alas, it isn’t that simple.

Yes, South Africa’s wind sector is growing. It had just 10MW of wind capacity installed at the start of this year, and the Global Wind Energy Council expects installations of up to 1GW this year. South Africa also has a target of developing 5GW of wind power by 2019.

It is good to see wind finally taking off in South Africa.

But most of its political leaders still see wind as a marginal concern. The ANC is keeping faith with coal despite the blackouts as it wants to exploit the country’s huge reserves. South Africa has the seventh-largest coal reserves in the world and gains more than three-quarters of its primary energy from coal. The ANC wants to make sure it extracts maximum value from this ‘black gold’.

This is why state-owned electricity utility Eskom is building the third- and fourth-largest coal-fired power stations in the southern hemisphere, called Medupi and Kusile, with total capacity of 9.6GW. They are due to start producing power this year, and a third plant of a similar size - Coal 3 - may follow.

Wind may be of little interest to Eskom or leaders with vested interests in the coal sector. But the election should still give hope to wind developers and investors.

We should not forget that the Department of Energy is providing support to the sector with mechanisms like its Renewable Energy Independent Power Producer Procurement Programme (REIPPPP). It is vital for South African wind businesses to demonstrate the value of the first wave of wind farms if support is to continue.

The industry should also be able to benefit from a public backlash where people are demanding a stable energy system by the time of the next elections in 2019. Companies in the wind sector should be able to demonstrate how wind farms can help make the energy network more diverse - and help to keep the lights on.

The ANC will come under major pressure to deliver a more stable and secure energy network. This gives an opportunity for those in the wind sector.

Yes, some prominent ANC backers have vested interests in coal, but ANC leaders also have a vested interest in getting re-elected. Energy security will be vital.

Pattern launches $400m public offering

Pattern Energy is looking to raise $400m with a public share issue, launched on Monday, to bolster its working capital and complete acquisitions.

This will enable the US developer to finalise deals including the acquisition of a 179MW interest in the 218MW Panhandle 1 project in Texas from its development arm Pattern Development. The $125m deal is due to complete next month.

The offering is being made through an underwriting group led by BMO Capital Markets, Morgan Stanley and RBC Capital Markets.

France will not back current GE-Alstom deal

The French government has said it would oppose General Electric’s $13.5bn takeover bid for Alstom’s energy arm over ownership concerns.

France's energy minister Arnaud Montebourg has written to GE chief executive Jeffrey Immelt saying that the government wanted a “balanced partnership”. This would be akin to the 50:50 joint venture between GE and aircraft engineer Safran, rather than a takeover that would see Alstom assets fall into the US firm's hands.

The government, in a letter published on Monday, said it would not back the current proposal because it would not be in France's interests. In a statement on Monday, GE responded that it is “open to continuing dialogue”.

$485m debt restructuring boosts Suzlon

Suzlon Group is poised to break even for the first time since 2011 after agreeing with its bondholders to restructure debts worth $485m.

The Indian manufacturer’s board agreed a restructuring of corporate bonds over the weekend. This has removed the threat of liquidation that has been a danger since October 2012, and means Suzlon could break even this financial year.

Suzlon has also signed an agreement with US developer PowerWorks Projects to supply 47 turbines totalling 99MW for schemes in California and Illinois.

Siemens scales K2 with 270MW deal

Samsung Renewable Energy has opted for Siemens turbines for its 270MW project K2 Wind in Ontario in Canada.

The developer has opted for SWT-2.3-101 turbines for the development, where commercial operation is scheduled to begin in spring 2015.

Siemens has also secured a ten-year service agreement with Pattern Energy, where it will service 405 onshore turbines in six projects in the US, Canada and Puerto Rico with a combined output of 930MW.

Gamesa secures 144MW Brazilian order

Eolicas do Sul, a subsidiary of Brazilian power company Eletrobas, has ordered144MW of Gamesa turbines for its Chui complex in southern Brazil.

The Spanish manufacturer is set to supply 72 of its G97-2.0MW turbines for the six wind farms that make up the complex, which is located in the state of Rio Grande do Sul. The project is due to be commissioned in the first quarter of 2015.

Gamesa has also announced an agreement to supply 48MW of turbines to China’s Fujian Energy in Dahanshan of Fujian Province in China.

For all the talk of boom and bust in the US market, it’s apt that AWEA 2014 opens in Las Vegas later today.

When the American Wind Energy Association unlocks the conference doors in the world’s gambling capital, it will enthuse about a US wind boom. More wind farms are being built in the US than at any time in history, it will declare. It is claiming a pipeline of 13GW.

But wait a moment before cashing in the chips and buying the casino’s most expensive bottle of Champagne. Here's our quick pre-conference reality check.

Yes, 13GW may be under construction, but that takes in all projects where any small element of work has already started on site. It does not mean that 13GW worth of turbines are going up across the US. And it doesn’t mean all of that 13GW will be built.

The reality is more sobering. Projects totalling 214MW were completed in the first quarter of 2014, and only 1GW was completed in the whole of last year. These are small numbers in a country with total installed wind capacity of 61GW.

Talk of a boom also ignores the fact that installations in the US fell more than 90% year-on-year in 2013 because of uncertainty in 2012 about the future of the production tax credit (PTC). The PTC was eventually extended through 2013 but it has now lapsed again.

In other words, this isn't the best time to be talking about a boom.

Developers and investors are now experiencing the same sort of uncertainty they felt back in 2012. The Senate has backed the extension of the PTC as part of the tax extenders bill, but Congress now has to decide whether this extension will happen. And there is no clear timetable on when this will happen.

The US market still relies heavily on the PTC and, if it isn’t extended, there won’t be any long-term boom.

Some analysts have suggested that as little as 2.5GW of new capacity would be added annually between 2016 and 2020 if the PTC is not extended.

We expect Congress to extend the PTC this time around, but we don't expect it to give any long-term commitment. It hasn't before. Relying on subsidies will make it tough for investors and developers to come up with long-term business plans.

There is a lot riding on the roll of the PTC policy dice, and it isn't the right time to suggest to legislators that everything is rosy.

Rather than tucking this under the carpet, at AWEA 2014 this week US wind businesses must take steps to improve the prospects for their schemes without betting on the support of the PTC.

For the most ambitious developers this should include courting the corporates, and securing deals like BNB Renewable did last week when it agreed a major power purchase agreement with Mars Corporation.

Deals like these can turn schemes that would be a gamble into a safe bet.

Wind Watch

For all the talk of boom and bust in the US market, it’s apt that AWEA 2014 opens in Las Vegas later today.

When the American Wind Energy Association unlocks the conference doors in the world’s gambling capital, it will enthuse about a US wind boom. More wind farms are being built in the US than at any time in history, it will declare. It is claiming a pipeline of 13GW.

But wait a moment before cashing in the chips and buying the casino’s most expensive bottle of Champagne. Here's our quick pre-conference reality check.

Yes, 13GW may be under construction, but that takes in all projects where any small element of work has already started on site. It does not mean that 13GW worth of turbines are going up across the US. And it doesn’t mean all of that 13GW will be built.

The reality is more sobering. Projects totalling 214MW were completed in the first quarter of 2014, and only 1GW was completed in the whole of last year. These are small numbers in a country with total installed wind capacity of 61GW.

Talk of a boom also ignores the fact that installations in the US fell more than 90% year-on-year in 2013 because of uncertainty in 2012 about the future of the production tax credit (PTC). The PTC was eventually extended through 2013 but it has now lapsed again.

In other words, this isn't the best time to be talking about a boom.

Developers and investors are now experiencing the same sort of uncertainty they felt back in 2012. The Senate has backed the extension of the PTC as part of the tax extenders bill, but Congress now has to decide whether this extension will happen. And there is no clear timetable on when this will happen.

The US market still relies heavily on the PTC and, if it isn’t extended, there won’t be any long-term boom.

Some analysts have suggested that as little as 2.5GW of new capacity would be added annually between 2016 and 2020 if the PTC is not extended.

We expect Congress to extend the PTC this time around, but we don't expect it to give any long-term commitment. It hasn't before. Relying on subsidies will make it tough for investors and developers to come up with long-term business plans.

There is a lot riding on the roll of the PTC policy dice, and it isn't the right time to suggest to legislators that everything is rosy.

Rather than tucking this under the carpet, at AWEA 2014 this week US wind businesses must take steps to improve the prospects for their schemes without betting on the support of the PTC.

For the most ambitious developers this should include courting the corporates, and securing deals like BNB Renewable did last week when it agreed a major power purchase agreement with Mars Corporation.

Deals like these can turn schemes that would be a gamble into a safe bet.

Wind Watch

For senior management at Alstom, General Electric and Siemens, it’s been quite a week.

Bloomberg revealed last Thursday that US giant GE was on the cusp of a takeover bid for French firm Alstom’s energy assets. This bid materialised on Wednesday. The French company has said it would make a decision on the GE bid by the end of May.

That makes it sound like the process has been straightforward. In reality, the GE takeover bid has provoked the ire of the French government, which doesn’t want one of its business jewels falling into US hands - or the secret talks that have surrounded the deal.

This anti-American rhetoric has now softened.

Meanwhile, GE’s German rival Siemens has complicated what looked to be a done deal by saying it would make a counter-offer. It now has four weeks to decide if it is going to do so after poring over Alstom's finances and interviewing its senior management.

The French government - which is not a shareholder in Alstom - has been more receptive to the idea of a Siemens takeover, and this could make it difficult for GE to finalise a deal.

All of this makes it look like Siemens is a shoo-in for a takeover, but that just isn't so. Our money's still on GE.

This month-long delay gives the government time to reflect on the absurd idea that an American firm is more likely to cut jobs than a German firm would. GE wants to grow in Europe and compete with Siemens, so it would make little sense for it to make major cuts even if Alstom's structure changes.

By contrast, Siemens is dominant in Europe and this gives it a far greater capacity to absorb Alstom into its existing operations.

The French government should also reflect on the negative message that scuppering the GE deal sends to international corporate cash. If the government is keen to attract renewable energy investors and create jobs, as environment and energy minister Segolene Royal said, it cannot be an obstacle.

We also see little evidence that a Siemens bid makes more sense. Siemens and Alstom have competed hard for decades, whereas GE and Alstom go back as far as 1928 with a shared founding company — as GE has already made clear.

Sure, for Siemens it would enable it to swap some troublesome transport assets, prevent GE gaining a major European foothold and eliminate one of its fiercest competitors.

But there are also reasons why doing no deal makes more sense for Siemens.

Talk of this bid may be a diversion that gives the company an opportunity to review Alstom’s finances in detail over the next month, as well as talking directly to its management.

And remember, Siemens hasn’t yet committed to bidding.

GE remains the favourite. Talks have been underway for months and for now, frankly, it’s the only real deal on the table.

For senior management at Alstom, General Electric and Siemens, it’s been quite a week.

Bloomberg revealed last Thursday that US giant GE was on the cusp of a takeover bid for French firm Alstom’s energy assets. This bid materialised on Wednesday. The French company has said it would make a decision on the GE bid by the end of May.

That makes it sound like the process has been straightforward. In reality, the GE takeover bid has provoked the ire of the French government, which doesn’t want one of its business jewels falling into US hands - or the secret talks that have surrounded the deal.

This anti-American rhetoric has now softened.

Meanwhile, GE’s German rival Siemens has complicated what looked to be a done deal by saying it would make a counter-offer. It now has four weeks to decide if it is going to do so after poring over Alstom's finances and interviewing its senior management.

The French government - which is not a shareholder in Alstom - has been more receptive to the idea of a Siemens takeover, and this could make it difficult for GE to finalise a deal.

All of this makes it look like Siemens is a shoo-in for a takeover, but that just isn't so. Our money's still on GE.

This month-long delay gives the government time to reflect on the absurd idea that an American firm is more likely to cut jobs than a German firm would. GE wants to grow in Europe and compete with Siemens, so it would make little sense for it to make major cuts even if Alstom's structure changes.

By contrast, Siemens is dominant in Europe and this gives it a far greater capacity to absorb Alstom into its existing operations.

The French government should also reflect on the negative message that scuppering the GE deal sends to international corporate cash. If the government is keen to attract renewable energy investors and create jobs, as environment and energy minister Segolene Royal said, it cannot be an obstacle.

We also see little evidence that a Siemens bid makes more sense. Siemens and Alstom have competed hard for decades, whereas GE and Alstom go back as far as 1928 with a shared founding company — as GE has already made clear.

Sure, for Siemens it would enable it to swap some troublesome transport assets, prevent GE gaining a major European foothold and eliminate one of its fiercest competitors.

But there are also reasons why doing no deal makes more sense for Siemens.

Talk of this bid may be a diversion that gives the company an opportunity to review Alstom’s finances in detail over the next month, as well as talking directly to its management.

And remember, Siemens hasn’t yet committed to bidding.

GE remains the favourite. Talks have been underway for months and for now, frankly, it’s the only real deal on the table.

Siemens reveals Alstom bid plan…

Siemens is set to bid for French firm Alstom’s renewable energy assets next month provided it is satisfied with due diligence.

The German manufacturer’s managing board and supervisory board said yesterday Siemens would bid for the assets in a deal reported to be worth around €11bn; but it needed four weeks to analyse Alstom’s finances and interview senior management.

The announcement followed interviews on Monday between the government and rival bidders Siemens and General Electric. The government is not a shareholder in Alstom but has intervened to protect French industry and jobs. France's rulers want Alstom to take a month to decide between Siemens and GE.

GE was reportedly close to a deal last week, but Siemens intervened with a counter-offer over the weekend. Alstom and GE officially announced a €12.35bn bid from GE this morning, and Alstom is set to decide whether to accept it by the end of May.

…as France plans post-nuclear strategy

French environment and energy minister Segolene Royal is set to propose new laws this July to help the country replace nuclear power with renewables.

Royal said she planned to accelerate investment in renewables, including wind, and that this would create 100,000 jobs by the end of 2017. France is aiming to reduce reliance on nuclear power from 75% now to 50% by 2025.

She is also set to this week announce the winner of a tender to develop 1GW in two wind farms off the French coast. Energy regulator CRE said last month that a group led by GDF Suez should win, but it faces competition from an EDF-led consortium.

Offshore trouble prompts ABB reform

Engineering firm ABB is to step up efforts to overhaul its power systems division due to problems in its offshore wind business.

The Swiss firm yesterday reported its power systems division had made a loss of €29m in the first three months of 2014. It attributed this to the impact of charges on delayed transmission projects in the offshore wind sector, particularly in Germany.

ABB is now reassessing its business model for offshore wind transmission projects. The company is set to hold its Annual General Meeting today.

Dakota turbine plane crash kills four

Four people have been killed after their plane hit a turbine on the 40.5MW South Dakota Wind Energy Centre in South Dakota.

The US Federal Aviation Authority has reported that the pilot of a single-engine aircraft and three passengers have been killed after hitting a 1.5MW General Electric turbine at the 27-turbine GE scheme. The wreckage was found on Monday.

The National Transportation Safety Board is investigating the crash, which is believed to have happened during foggy weather.

Greenko opts for 100MW from Gamesa

Indian wind power developer Greenko has ordered 50 of Gamesa’s G97-2.0MW turbines for projects in the Indian states Andhra Pradesh, Karnataka and Rajasthan.

The developer made the 100MW order under a 300MW framework agreement concluded in 2013. Gamesa will also provide operation and maintenance services for five years.

The projects are due to be commissioned by March 2015.