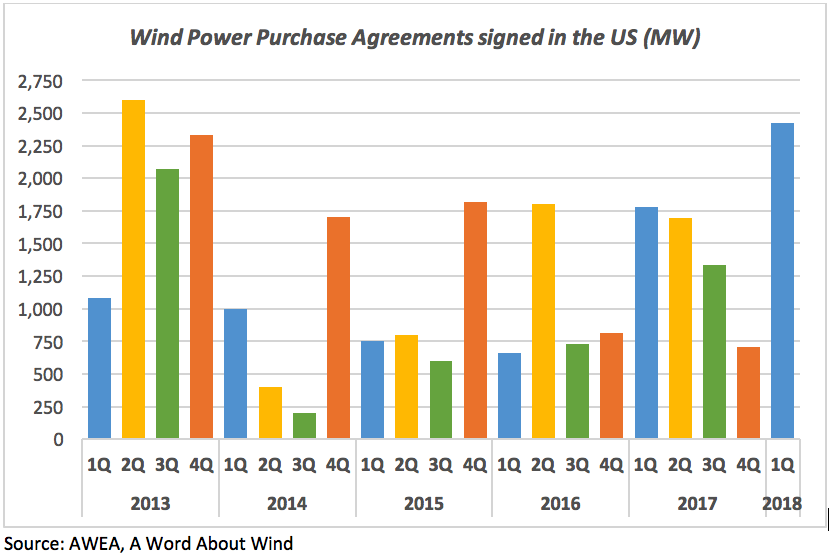

Wind farm owners concluded power purchase agreements totalling 2.4MW in the US in the first quarter of 2018, according to A Word About Wind research on reported deals. This makes the first three months of 2018 the strongest quarter in almost five years.

Our latest Finance Quarterly report, which is due out on Tuesday, shows that energy buyers are committing to wind PPAs despite political uncertainty and falling wholesale power prices in the US.

Corporates and other non-utility customers have driven the strong result of this quarter, signing for over half of the capacity contracted (1.3GW). Utilities have agreed to buy the other 1.1GW.

Major corporates including AT&T and Facebook have been among the biggest buyers of wind energy in the three months ending in March. In particular, telecoms giant AT&T agreed to purchase the total output of two wind farms, developed by NextEra Energy in Texas and Oklahoma, with total capacity of 520MW.

Social media giant Facebook signed wind PPAs to buy 336MW of power produced by three projects totalling 536MW. This includes a deal to gradually purchase 120MW of wind power of the 320MW Rattlesnake Creek wind farm by 2029, in addition to the 200MW that the firm already agreed to buy from the project in Q4 2017. It is set to use the electricity to power a data centre in Nebraska.

The nine corporates that confirmed they had signed PPAs included first-time buyer Jack Daniel's maker Brown-Forman, which agreed to purchase 30MW of the 474MW Solomon Forks wind farm in Nebraska. This was the first commitment to buy renewable energy by a spirits and wine producer in the US.

The volume of PPA deals signed in the first quarter of 2018 shows that PPAs represent the most powerful tool that wind developers in the US have to secure construction of their projects. Despite the election of President Donald Trump and cheaper wholesale power prices, companies keep seeing wind as a strategic investment to diversify their energy portfolio and secure long-term sustainability.

It is still early days but, if companies keep up this momentum, 2018 may be the US wind industry's strongest year yet for PPA deals.

Wind watch is published every Monday, Thursday and Friday.

In the meantime, have you checked out the latest posts on our blog? We've got some interesting additional pieces on there.

For our series of member Q&As, Frances Salter spoke to Julien Sellier, managing director of Structeam. Here's an excerpt, and you can read the full piece here. If you'd like to take part in a member Q&A, email us at editorial@awordaboutwind.com.

Member Q&A: Julien Sellier, Structeam

In the simplest terms, what does your company do?

We are consultants in blade technology, as well as being contractors. This means we are specialists in advanced materials such as fibre re-enforced plastics and the technology used to make blades cost-effectively. We work in Europe, India and China.

Of the deals you’ve worked on, which is your favourite and why?

I have many favourites: one would be when we got our first blade design in 2011, which was certified through DNV-GL. The main achievement was to convince this first customer that we would deliver with our newly formed company, and we delivered; that’s why it was is so symbolic for the company.

In which markets do you see the biggest opportunities right now?

Probably China has the lion’s share, but Europe and America are also significant.

What do you think is the biggest challenge facing the wind industry, and how would you solve it?

I think it’s operations and maintenance because the investment phase is now well understood. The little operations and maintenance problems become bigger as the industry grows. We have to remember that 10 years ago, 2MW turbines were the largest platform available: now it is in the region of 6-8MW. This scalability...

BlackRock’s David Giordano is set to take over as the chair of the ACORE board of directors in June. He are some of his key insights into investment trends in the US wind market.

BlackRock’s David Giordano is set to take over as the chair of the ACORE board of directors in June. He are some of his key insights into investment trends in the US wind market. David will be speaking at our Financing Wind New York conference on 30th May: for more info and to book tickets, see our conference website.

“The Clinton administration wouldn’t have been as positive [for renewables] as some people might have thought, and the Trump administration is not as negative."

That is a view of David Giordano, head of renewable power in the Americas and Asia-Pacific at global investment giant BlackRock, which he shared with A Word About Wind in the sixth edition of our annual Top 100 Power People report in November. He gave us his insights on policy and investment in US wind after the close of a $1.65bn wind and solar fund last July.

And his insights will take on greater weight in the sector in June, when he is set to step up to replace Dan Reicher as chair of the American Council on Renewable Energy (ACORE) board of directors. ACORE president Gregory Wetstone said last month that Giordano’s elevation to this pivotal role in one of the leading US trade associations reflected the importance of finance to booming US renewable energy industry. We can only agree.

In light of his elevation at ACORE, we thought it’d be a good time to revisit what we learned from David during our interview. Here are three of the most important points – and, if you’d like to read the full interview, we’re now making it available to everyone in our free e-book:

Donald Trump’s impact on US wind has not been as negative as some feared

Despite President Trump’s famed objection to wind farms, David argued that he had not been a particularly obstructive figure for the wind industry since entering the White House – perhaps because wind now supports over 100,000 US jobs, many of which are in the manufacturing sector in Republican heartlands.

He has also not shown any appetite for a faster reduction in the wind production tax credit, which is set to come to an end in 2019 – and was protected in a package of US tax reforms that came into force in January, following our interview. In any case, support for the US wind sector largely comes at the state- and city-level.

Fixing transmission is one of the industry’s most pressing challenges:

David highlighted the need for grid improvements, so that low-cost wind energy can be moved from the best wind sites – which tend to be in remote areas in the heart of the country – to cities where it is most needed, including on the coasts.

He also discussed the difficulty of building the required transmission lines, because the projects need support from affected states and landowners. However, he said he didn’t think funding them would be a problem: plenty of investors are interested in transmission investments but, for progress to be made, government support for developers will still be needed.

There are still considerable limitations to offshore wind in the US:

David said BlackRock was considering making investments in offshore, particularly on the east coast, but was waiting to see “material growth” in the sector. He said that, while there is currently a lack of an offshore wind supply chain and supporting infrastructure, he expects to see offshore wind farms built off the US east coast due to the density of population, the demand for power and the constraints on capacity.

We have since seen plenty of activity to back up the theory, with NYSERDA setting out its roadmap for the state to reach 2.4GW of offshore wind capacity by 2030. In total, east coast states have targets for 8GW of offshore capacity.

European businesses may baulk at the prospect of President Trump’s protectionist policies hitting the nascent offshore wind sector, but a new bill in Congress will help US workers to share in the benefits of the sector. Richard Heap reports

European businesses may baulk at the prospect of President Trump’s protectionist policies hitting the nascent offshore wind sector, but a new bill in Congress will help US workers to share in the benefits of the sector. Richard Heap reports

At A Word About Wind, we are due to publish our debut North American Power List at our Financing Wind New York conference on 30th May. But before that, we have exciting news about our cover interviewee and top individual: US President Donald Trump.

Happy Easter -- and Happy April Fool's Day. We hope you enjoy seeing The Donald on the cover of North American Power List but, rest assured, we'll publish the real list on 29th May and share it at Financing Wind New York.

At A Word About Wind, we are due to publish our debut North American Power List at our Financing Wind New York conference on 30th May. But before that, we have exciting news about our cover interviewee and top individual: US President Donald Trump.

President Trump has had a stormy relationship with those in the wind market. This includes disputes about projects in Scotland and the Republic of Ireland; and repeat attacks on their efficiency and environmental credentials. Wind feared the worst when he was elected.

Really, though, we needn’t have worried. Despite initial fears, the wind industry has carried on its strong growth under Trump’s leadership. And so we’re delighted that The Donald has agreed to speak to our editor for this report, which we’ll launch in New York on 30th May.

“I want to thank – you know, I’ve had a lot to say about wind farms, killing birds… so many, many birds. Terrible. But I’m glad to speak to World Of Wind,” he told A Word About Wind. “These wind people are great people. Very, very good people. True American patriots.”

Last year, wind farms totalling over 7GW were completed in the US, and the industry now supports over 100,000 jobs across all 50 states, according to official industry statistics. This is a testament to the great work that President Trump did in protecting the wind industry during tax reforms, and the reason we’re pleased to share this accolade at our event.

Financing Wind New York will be held at 237 Park Avenue in New York on 30th May, and we have a strong line-up of speakers – and we fully expect President Trump to join us too.

Our confirmed speakers include Ray Wood from Bank of America Merrill Lynch; Nick Knapp from CohnReznick Capital; Hannon Armstrong’s Susan Nickey; NYSERDA’s Alicia Barton; and Jatin Sharma from GCube Insurance. Here’s the full line-up: http://financingwind.com/

Our events are open to A Word About Wind premium, gold and silver members; and tickets include access for you or a colleague to our annual Financing Wind conference in London in late 2018; six Quarterly Drinks evenings in London and New York; and all of our editorial too. That includes access to the North American Power List that we’ll release at that event.

“Looking at our growth, I’m delighted to be able to meet a businessman of Trump’s calibre – and I’m sure the feeling’s mutual,” said Adam Barber, publisher of A Word About Wind and founder of the Tamarindo Group. “We’re delighted to be hosting our debut event in The Big Apple, and the thing is that nobody represents New York like President Trump.”

So what are you waiting for? Don’t be an April fool. Check out the full details here today: http://financingwind.com/

Japan has spent years talking about offshore wind – and with little to show for it. Its government started looking at renewable energy in the aftermath of the Fukushima Daiichi nuclear disaster in 2011. This opened up opportunities for developing offshore wind farms.

In a report published last year, the consultancy Institute for Energy Economics & Financial Analysis identifies the potential for 10GW of offshore wind in Japan by 2030. And in December, the Japan Wind Power Association estimated the potential to install offshore wind farms in Japanese waters with a total capacity of 100GW.

However, the government has been slow to introduce laws and regulations to ease the development of offshore wind, and the nation is far from unleashing its potential.

Despite its renewables push in the last seven years, Japan has installed only 60MW of offshore wind projects so far. This delay is leaving the country lagging behind its neighbours, particularly neighbouring Taiwan, which has set aggressive renewable energy targets and aims to build 5GW of offshore wind farms by 2025.

That isn’t to say Taiwan has got everything sorted. It is taking the steps it needs to build an offshore wind industry, and the excellent wind resources and government commitment have brought in foreign investors including Ørsted, Copenhagen Infrastructure Partners, Macquarie and Wpd. There is a lesson here for Japan.

And this slow growth is despite the fact that Japanese investors have already shown interest in the offshore wind industry. Falling costs and Japanese interest rates at a record low of -0.1% since January 2016, have pushed investors to look at offshore wind investments in Europe for stable, long-term revenues.

For example, this week Japanese conglomerate Mitsubishi has bought a 33.4% stake in the 950MW Moray East in UK waters; and is reportedly looking to invest in the 370MW Norther off the Belgian coast and the 130MW Luchterduinen off the Dutch coast.

Meanwhile, Japanese investment firm Marubeni this week disposed of its stake in the 210MW Westermost Rough, which acquired in 2015, as it seeks to focus more on its home market.

Other key players include Japanese bank MUFG, which in 2017 financed 63 clean energy and energy-smart technology projects, totalling $4.3bn. Its investments in offshore wind include the refinancing of the 288MW Butendiek offshore wind farm, and the financing of the 588MW Beatrice and the 332MW Nordsee One.

These are just few examples but they demonstrate the interest Japanese firms have shown in the European offshore wind industry, and how Japan could make use of their experience if it had a framework that allowed it do so. But it doesn’t.

One reason for Japan's slow growth is that many projects in its waters will need to use floating foundations, which have not yet been proved as commercially-viable for utility-scale projects.

But the main reason for Japan’s slow progress has been a lack of national legislation for offshore wind, which has brought various prefectural governments to implement their own local rules. This means the rules vary substantially between prefectures, and has made the development process long, difficult and confusing.

The country is looking to change this. In January, Prime Minister Shinzo Abe announced that the government would introduce new laws to use Japanese waters for offshore wind.

Following that, the cabinet approved this month legislation to allow developers to place competitive bids to win the rights to develop offshore schemes. The law is due to go through the Japanese Diet by the end of May.

Competitive tenders would help to accelerate the development of an offshore wind market in the country and drive down costs. The offshore wind feed-in tariff is currently ¥36,000/MWh (€274/MWh), which is four times higher than the €65.60/MWh (£57.50/MWh) at which the 1.4GW Hornsea 2 and 950MW Moray East schemes won support in the UK in September. It needs to come down.

It’s good to see that the Japanese government is taking steps to promote offshore wind, but there are years of delay to overcome. The solution could lie in learning from Japanese corporations with offshore experience, and its neighbour Taiwan. After taking seven years to go nowhere, things might now finally start moving.

We maintain it’ll be vital for the US to learn from firms in Europe and Asia about how to keep down the cost of offshore wind farms.

But as Jatin Sharma, president at GCube Insurance Services, said on our LinkedIn post about that article, there would also be benefits to policies that help US firms to share the financial success of the industry. He wrote: “US offshore needs to find a balance between LCOE and the political buy-in needed to help it flourish.”

In other words, there’s a place for some protectionism, as long as it doesn’t do major damage to the economic case for offshore wind. If people can see there are financial benefits of offshore wind for them and their families, they’re more likely to support it. This can help to reinvigorate communities, with cities such as Grimsby and Hull in the UK embracing offshore wind for that reason.

It’s with this in mind that we were interested to hear this week about the plan for the Offshore Wind Jobs & Opportunity Act in the US – but, rather than a standalone bill, it would require an amendment to the Outer Continental Shelf Lands Act. You can find out more about the technical details of the proposal here.

In summary, Democrat members of Congress in Arizona and Massachusetts introduced this legislation in a bid to help workers adapt to the growth of US offshore wind.

They propose to do this by offering grants to governments, unions and universities to help people re-train; with a focus on displaced workers from the offshore oil and gas, onshore fossil fuel, nuclear and fishing industries. It would also support other groups including military veterans. All of these groups could bring useful skills.

Massachusetts Congressman Bill Keating used the launch of the plan to blast repeated attacks on wind by the Trump administration. He said: “Despite this administration’s attacks on clean energy, there are plenty of hard-working Americans who are ready, willing and able to train in the wind industry… [This] legislation will help us meet our goal of ensuring that we have a well-trained, local workforce ready on day one.”

The plan’s other supporters include the American Wind Energy Association, National Wildlife Federation, the Utility Workers Union of Americas, and United Steelworkers.

No doubt it would be welcomed by companies in the sector as well. For turbine makers such as General Electric, MHI Vestas and Siemens Gamesa, it would give them access to a pool of skilled offshore wind workers. This will be important when they decide whether to invest in new factories to build their platforms in the US.

And it should open opportunities for specialists in Europe and Asia to help provide training. Where better to get offshore wind expertise than from the markets with most practical experience?

So what happens next? Well, the bill was introduced on 14 March by Massachusetts Congresswoman Niki Tsongas, and it still needs to be considered in the US House of Representatives by the Committee on Natural Resources and the Committee on the Education of the Workforce.

If it passes that there it could be considered by the full House, and would need approval from the House, Senate and president.

There’s a long way to go. But, as the US offshore wind sector seeks to make friends, it feels like a road worth taking. After all, nobody can object to job creation, right?

You can hear more from Jatin Sharma and a host of other North American wind industry experts at our Financing Wind New York conference, in association with GCube Insurance Services, on 30thMay. Check out the full details here: www.financingwind.com

In our most popular blog post this week, Alice Jones looks at the key risks that can pose a threat to the profitability of wind projects. Here's an excerpt, and you can read the full piece here.

The 6 biggest risks to wind farm profitability By Alice Jones

When deciding whether to invest in a wind farm, there are numerous considerations that companies must take into account – financial backing, legal requirements, local regulatory policy, calculating predicted revenue, and so on.

And as well as these considerations, there are also a host of other risks that can pose a threat to the profitability of projects. As the cost of wind power tumbles and project owners’ margins are squeezed, these risks could potentially be very damaging.

In this article, we outline the six biggest risks to your wind farm revenue – and what you can do to protect against them.

1) NATURAL CATASTROPHES

Anyone who read the news in 2017 did not have to look far for a natural catastrophe (‘nat cat’ to your insurers). During the summer, hurricanes Harvey, Irma and Maria wrought havoc across the US and Caribbean; Mexico suffered three earthquakes in September alone; and wildfires blazed across California during the autumn.

Meanwhile, Afghan avalanches, South Asian monsoon floods, and an earthquake on the Iraqi-Iranian border claimed hundreds of lives. In addition to their devastating human impacts, the costs of natural catastrophes for renewables projects including wind farms is high – and countries that combine high ‘nat cat’ exposure with a high density of renewables projects are most vulnerable.

Naturally, both should be a concern for those investing in the US wind sector, and it may be tempting to see the first as the bigger issue. Undoubtedly, if hackers can disrupt the electricity system then that could hit production at wind farms, or cause blackouts in the whole grid, and have a significant impact on wind farm owners.

However, given all the discussion this month about the use of social media to influence elections, we’re more intrigued by the trolls.

The House of Representatives investigation says that the Kremlin-linked Internet Research Agency – a troll factory – put thousands of posts on Twitter, Facebook and Instagram from 2015 to 2017 in order to stir up controversy about US energy policy. The aim was to help Russia to achieve its geopolitical goals.

And this is where it gets interesting for wind investors. On one hand, the Russian government has been looking to these trolls to promote messages that support de-carbonisation, which includes talking up the potential of wind farms; and, on the other, it has been looking to ramp up the debate about climate change by showing it as a ‘liberal hoax’. Why take up these two conflicting positions?

Well, Russian foreign policy is never simple. In 1939, Winston Churchill famously referred to the county as “a riddle wrapped in a mystery inside an enigma”, and it is no different under the leadership of Vladimir Putin. Even so, we'll give it a go.

In supporting de-carbonisation, the trolls were looking to make the case for ‘alternative’ sources, including wind and solar farms, in a bid to head off US support for shale gas fracking. This includes amplifying messages from green groups that it felt might be able to stop the use of fracking – and so keep the US reliant on Russia for fossil fuels. This may be beneficial for the wind industry but it still makes sense for investors to be aware of who their friends are and why.

Not that it worked. Since 2014, the US shale gas revolution has helped to drive down crude oil prices from over $100 a barrel to under $60, which has hit Russian energy interests. And the wind sector has also seen strong growth in the US since the extension of the production tax credit for the wind sector in late 2015. These are turning the US from a net energy importer into a net exporter.

Meanwhile, in spreading doubt about climate change, the trolls were seeking to sow discord in the debate about US energy policy; and breed public discontent in policies being pursued by political ‘elites', including fracking. It’s a familiar trope from recent UK and US elections, and we expect this part of the battle to continue.

And despite the evidence, there will be an enduring debate about climate change and the extent to which human beings are responsible for it. Social media will make sure of that. While it may enable people from around the interact with each other, it also gives a perfect vehicle for conspiracy theories to take root, and help people to reinforce their opinions rather than to alter them.

There are steps that can be taken to protect energy investors. The US government is aware of Russian attempts to influence the energy market, and said it’s committed to running a market free from overseas interference. This doesn't mean it will be able to control the discussion, but at least it's aware of the threat. That’s a start.

The other good point for wind investors is that support for wind and other renewables is not just about climate change any more. The falling cost of wind power means the industry’s prospects are now tied more to price and reliability than green concerns.

It won’t stop the information war – but, for now, should give US wind operators some protection from it and confidence in wind’s long-term prospects.

Swedish utility Vattenfall has won the right to build two wind farms totaling 700MW in Dutch waters with no government subsidies. However, a headlong rush to zero-subsidy projects could make life tougher for wind businesses. Richard Heap reports

Swedish utility Vattenfall has won the right to build two wind farms totaling 700MW in Dutch waters with no government subsidies. However, a headlong rush to zero-subsidy projects could make life tougher for wind businesses. Richard Heap reports

It was a good day to bury bad news. Last Monday, Swedish utility Vattenfall set out plans to cut 1,500 jobs from its 20,000 workforce. However, the firm also celebrated a win in the Dutch government’s 700MW Hollandse Kust 1 and 2 offshore auction – and the latter story dominated wind industry headlines last week.

The two projects, each set to measure 350MW, are all the more notable because they could be the first zero-subsidy offshore wind farms completed anywhere in the world when they complete, due in 2022. The zero-subsidy projects awarded support in the first German offshore wind auction last year are not due until after 2024. This could be an exciting period for the wind industry.

And yet, we see reasons to be concerned about the rush towards ‘zero-subsidy’ offshore wind farms. Some of these were summed up neatly by Scottish Power CEO Keith Anderson during an Aurora Energy Research conference in the UK last week.

He said he hated the phrase ‘subsidy-free’ and can’t see why the industry is becoming “obsessed” with it. It means that wind farm owners will be relying solely on wholesale power prices, which is a risk he said he isn’t prepared to take.

“If you’re looking at building a £2.5bn offshore wind farm in the UK, if you think I’m going to do that at market risk, you’re bonkers,” he said. “In the UK, nothing in this industry [i.e. the energy industry] is built without some sort of support.”

Equinor’s Irene Rummelhoff gave a similar warning last September that zero-subsidy projects could “ruin the reputation of the industry” if they’re not done successfully – although she did say in December that the company had submitted a zero-subsidy bid in this Dutch auction. It isn’t a path that Scottish Power, which is owned by the Spanish utility giant Iberdrola, is keen to follow.

Anderson said that going ‘zero-subsidy’ raised the risks for wind farm owners, or pushed them to try to secure corporate power purchase agreements – even though deals big enough to support offshore wind farms don’t exist. He said the UK should continue to support offshore wind farms via Contracts for Difference, as well as new onshore wind farms, because they give long-term certainty to the wind farm owner and the government. This kind of long-term government support is important.

And Vattenfall CEO Magnus Hall also backed the use of CfDs.

We can see why the wind industry is keen to shout about ‘zero-subsidy’ schemes. It shows that the offshore wind sector is becoming even more competitive with other energy sources. However, it could also push operators into an impossible corner.

For one, it suggests many people in the wind industry don’t know how best to engage with the debate on government support for schemes, whether that is in the form of subsidies, CfDs or other mechanisms. And we can see why: for years, wind has been a victim of critics who argue wind farms are unreliable, and can only be profitable if their owners receive huge public subsidies. People in the industry have been working hard to address these criticisms – and have made good progress too.

Now wind farms are more predictable and costs are lower than ever, and we can see the temptation to say: ‘Actually, we don’t need subsidies now, so there.’

But why get drawn in? Almost every UK power plant receives subsidies, and any new fossil fuel plant would too. It’s a victory for the fossil fuels sector that the debate around subsidies and constraint payments is always about how they are paid to wind farm operators, when fossil fuels benefits from the exact same thing.

And yet, despite those headlines, renewables enjoy strong support. Official figures from the UK government show 82% of people in the UK back the use of renewables, and 79% support offshore wind specifically. Most don't care about the payments.

What we need is a sensible discussion over government support for all sectors, not that we'll get it. What we don’t need is the wind industry boxing itself into a corner where it won't be able to accept help again. Wind’s main message should be that it delivers stable, long-term, low-cost and clean energy, and so needs stable market mechanisms to continue doing that.

Because, for the industry’s critics, ‘zero-subsidy’ won't be virtuous enough. In the Dutch auction, no doubt much will be made of the fact Vattenfall isn’t paying for the grid link and that’s still a form of support. The wind farm haters won’t just go away.

And those in the wind industry in the UK should also make the point that the country has committed to de-carbonise its energy mix. Using renewables is one way to help do this, and that stable support is the way to achieve this, not market uncertainty.

We’re sure Vattenfall has done its sums. However, our worry is more firms might be bounced into agreeing ‘zero-subsidy’ deals that give them little certainty over long-term returns from merchant power prices, or from PPAs where the counterparty might not be around in 20 years’ time. These are big risks to the sector’s long-term reputation – and all to avoid making the blindingly obvious point that wind deserves the same support as other sectors.

It was a good day to bury bad news. Last Monday, Swedish utility Vattenfall set out plans to cut 1,500 jobs from its 20,000 workforce. However, the firm also celebrated a win in the Dutch government’s 700MW Hollandse Kust 1 and 2 offshore auction – and the latter story dominated wind industry headlines last week.

The two projects, each set to measure 350MW, are all the more notable because they could be the first zero-subsidy offshore wind farms completed anywhere in the world when they complete, due in 2022. This could be an exciting period for the wind industry.

And yet, we see reasons to be concerned about the rush towards ‘zero-subsidy’. Some of these were summed up neatly by Scottish Power CEO Keith Anderson during an Aurora Energy Research conference in the UK last week.

He said he hated the phrase ‘subsidy-free’ and can’t see why the industry is becoming “obsessed” with it. It means that wind farm owners will be relying solely on wholesale power prices.

“If you’re looking at building a £2.5bn offshore wind farm in the UK, if you think I’m going to do that at market risk, you’re bonkers,” he said. “In the UK, nothing in this industry [i.e. the energy industry] is built without some sort of support.”

Equinor’s Irene Rummelhoff gave a similar warning last September that zero-subsidy projects could “ruin the reputation of the industry” if they’re not done successfully.

Anderson said that going ‘zero-subsidy’ raised the risks for wind farm owners, or pushed them to try to secure corporate power purchase agreements – even though deals big enough to support offshore wind farms don’t exist. He said the UK should continue to support offshore wind farms via Contracts for Difference, as well as new onshore wind farms, because they give long-term certainty to the wind farm owner and the government.

And Vattenfall CEO Magnus Hall also backed the use of CfDs.

We can see why the wind industry is keen to shout about ‘zero-subsidy’ schemes, but we feel like it also risks pushing operators into an impossible corner.

For one, it suggests many people in the wind industry don’t know how best to engage with the debate on government support for schemes, whether that is in the form of subsidies, CfDs or other mechanisms. And we can see why: for years, wind has been a victim of critics who argue wind farms are unreliable, and can only be profitable if their owners receive huge public subsidies.

Now wind farms are more predictable and costs are lower than ever, and we can see the temptation to say: ‘Actually, we don’t need subsidies now, so there.’

But why get drawn in? Almost every UK power plant receives subsidies, and any new fossil fuel plant would too. It’s a victory for the fossil fuels sector that the debate around subsidies and constraint payments is always about how they are paid to wind farm operators, when fossil fuels benefits from the exact same thing. And yet, despite those headlines, renewables still enjoy strong support. Most people don't care about the payments.

What we need is a sensible discussion over government support for all sectors, not that we'll get it. What we don’t need is the wind sector boxing itself into a corner where it won't be able to accept help again. Wind’s main message should be that it delivers stable, long-term, low-cost and clean energy, and so needs stable market mechanisms to continue doing that.

Because, for the industry’s critics, ‘zero-subsidy’ won't be virtuous enough. In the Dutch auction, no doubt much will be made of the fact Vattenfall isn’t paying for the grid link and that’s still a form of support. The wind farm haters won’t suddenly go away.

We’re sure Vattenfall has done its sums. However, our worry is more firms might be bounced into agreeing ‘zero-subsidy’ deals that give them little certainty over long-term returns from merchant power prices, or from PPAs where the counterparty might not be around in 20 years’ time. These are big risks to the sector’s long-term reputation – and all to avoid making the blindingly obvious point that wind deserves the same support as other sectors.

With just a couple of months to go until Financing Wind New York, here's a round-up of our key speakers. For more information and to book tickets, visit our conference website: www.financingwind.com

There are just a couple of months to go until Financing Wind New York, where we'll be discussing the most important issues in the US wind market with a host of top names. Here are 12 people that you'll be able to hear from.

It's now just two months until our first US conference on 30th May, which we are hosting with our headline sponsor GCube Insurance Services, and tickets are going fast! You may have seen our speaker announcements on LinkedIn, and here's our complete run-down of the speakers we've announced to date.

1. Alicia Barton

Our keynote speaker, Alicia Barton, is president and CEO of the New York State Energy Research & Development Authority (NYSERDA). She's worked in leadership roles in public and private clean energy projects for over a decade. In her current role at NYSERDA, she is leading efforts to make New York a global hub for offshore wind.

2. Nick Knapp

Nick Knapp, President of CohnReznick Capital, will also be speaking. Nick primarily focuses on M&A buy-side and sell-side and raising, structuring and negotiating tax equity investments, with a core focus on utility scale wind and solar projects.

3. Shalini Ramanathan

We're also looking forward to hearing from Shalini Ramanathan of RES Americas. Shalini joined the US subsidiary of the RES Group in 2007 as a project developer and rose to vice-president of development before moving to vice-president of origination in 2014. During her career, she has closed deals worth $2.5bn on wind, solar and energy storage projects totalling 1.5GW, and negotiated off-take agreements with firms including General Motors, Google, Microsoft and Xcel Energy.

4. Ted Brandt

Ted is CEO of Marathon Capital. He co-founded the company in 1999 to provide independent investment banking and financial advisory services in the North American wind industry. In those 18 years it has advised on more than 100 projects.

5. Susan Nickey

Susan is Managing Director at Hannon Armstrong, and is also on the board of directors at AWEA. She has been instrumental in Hannon Armstrong's minority investments totalling approximately $400 million in a diversified portfolio of wind projects, with a total capacity of over 2,500 MW.

6. Steve Lockard

Steve joined TPI, the world's only major independent blade manufacturer, in 1999 and became its president and CEO in 2004. TPI, based in Arizona, has secured key overseas transactions in the last year which include long-term deals with Siemens Gamesa in Turkey; with Vestas in Latin America; and with Senvion in Asia-Pacific and Latin America.

7. Rob Threlkeld

Rob is Global Manager of Renewable Energy at General Motors, leading the company's efforts to deliver its operations using 100% renewable energy by 2050. He manages its growing portfolio of renewables and leads the development of new projects to meet sustainability goals.

8. Rob Freeman

Rob is a CEO and founding member of developer Tradewind, which was established in 2003 with backing from local angel investors. In 2006, he led the firm as it teamed up with Italian utility Enel, and the pair have since completed wind and solar projects worth over $5bn in the US.

9. Declan Flanagan

Declan is CEO of developer Lincoln Clean Energy, which he set up in 2009 and led through its acquisition by I Squared in late 2015. His highlights of last year included completing a 253MW wind farm for Amazon in Texas, where Amazon CEO Jeff Bezos was famously photographed standing on a turbine smashing a bottle of Champagne.

10. Jatin Sharma

Jatin joined specialist renewables insurer GCube Insurance Services in 2010, and was promoted to president of its North American operation in January. He specialises in underwriting offshore wind, wave and tidal projects; and is a recognised thought leader on the insurance side of the wind sector.

11. Ray Wood

Ray has built a reputation as a big dealmaker in the US wind market thanks to almost three decades’ experience in investment banking, including more than 20 years specialising in energy. He spent 22 years at Credit Suisse before joining Bank of America Merrill Lynch in 2012, where he is now Global Head of Power and Renewables.

12. Jayshree Desai

Jayshree is Chief Operating Officer at Clean Line Energy Partners LLC, and has been an independent director of TPI Composites since September 2017. She previously spent 7 years directing corporate and project finance for Texas-based firm Horizon Wind Energy.

We are hosting Financing Wind New York is partnership with headline sponsor GCube Insurance Services, gold sponsor Marathon Capital, silver sponsor Tamarindo Communications, and supporting organisation Tradewind Energy.

When I was little, I dreamt of working at Italian oil giant Eni. My father used to work there and, for me, Eni was a magic world of trips on helicopters with my dad, to reach offshore platforms where kind men used to give me toys and candies. No wonder I wanted to work there! Then I grew up, came to the UK and joined AWAW… things have clearly changed. [Not as many kind men here? - RH]

When Eni’s chief executive Claudio Descalzi presented the state-owned utility’s four-year plan last week, Italian media praised the commitment to renewables shown by the world’s 14th largest oil company. But a closer look reveals that Eni is only taking early steps in the renewables sector and there is still a long way to go before it could achieve a proper green transition. Let’s look at its involvement in renewables so far.

In 2015, Eni founded a division called ‘energy solutions’ with goals to cut emissions, develop renewables projects, and promote use of gas. It has so far built only 63MW of renewable energy capacity.

The oil firm got involved in renewables again in 2016 when it signed an agreement with General Electric to develop large renewables projects in Italy, with onshore wind its preference. We haven’t yet heard any more about this, but the first joint project of the partnership should be announced this year.

And finally, last year Eni signed a two-year framework agreement with Norwegian oil company Statoil – now Equinor – to identify and develop new projects in order to integrate renewable energy solutions in the existing oil and gas fields.

But Eni’s 2018-2021 strategic plan is its most significant commitment to renewables so far. The Italian firm is set to invest €1.2bn to develop 1GW of new wind and solar capacity by 2021. This includes 700MW of new wind and solar projects in emerging markets where the Eni is already well-established, with a particular focus on Africa, and up to 220MW of new capacity in Italy. The firm aims to bring its renewable energy portfolio to 5GW by 2025, although oil and gas will remain its core business.

In fact, the €1.2bn investment in renewables is part of a €32bn plan, of which more than 80% will be dedicated to its fossil fuels extraction business. In particular, Eni is set to invest €3.5bn to drill up to 115 new oil fields in 25 countries. This is far more ambitious than its plan for renewables – and shows that energy transition is still a long way off. As people get more savvy about greenwashing, Eni would be well-advised to not over-promise on its green plans.

It is not the first to seek to strike this balance. We have seen other oil companies, including Engie, Shell, Statoil and Total looking with more interest at investments in renewables over the last decade, while keeping their business focus on fossil fuels.

And yet, Eni’s commitment to renewable energy is also very limited if compared to those other major players. Why is that?

Well, Eni’s oil drilling operations, in particular in the neighbouring African regions, are vital for Italy. The state-owned company has been drilling in Africa since 1950 and its activity there is key to satisfy Italy’s energy needs. Italy imports 86% of its energy, and oil and gas account for around 65% of the Italian energy mix. The country could not cope with a reduction of Eni’s oil and gas fields.

The 700MW of wind and solar projects that Eni plans to build in emerging markets, including in Africa, could represent a turning point for the company’s renewables business.

The oil firm is well-established in Africa and a renewable energy investment in the region would take advantage of its knowledge of the territory. It has potential but, for Eni, a major shift to renewables is still a long way off – and isn’t yet big enough to reignite that child-like sense of wonder I once had.

Greencoat Capital managing partner Richard Nourse told editor Richard Heap about his views on overseas investment, Brexit and storage at Quarterly Drinks this month.

Greencoat Capital managing partner Richard Nourse told editor Richard Heap about his views on overseas investment, Brexit and storage at Quarterly Drinks this month.

On 7th March, we hosted our first Quarterly Drinks evening of 2018 at The Shard in London, and heard interesting views on the market in our interview with Richard Nourse, managing partner at UK infrastructure investor Greencoat Capital.

Nourse calls himself a ‘recovering banker’ after working for two decades at Morgan Grenfell and Merrill Lynch. He then set up Greencoat Capital in 2009. The firm now has at least £2bn of assets under management in wind, solar and private equity; and this gives Nourse a great view on investment trends in wind.

Here are five of his key points:

1) Greencoat is focused on expanding in Ireland…

The firm’s flagship fund is Greencoat UK Wind, which invests in operating onshore wind farms in the UK and now has a portfolio of £1.25bn. Last week, it paid £163m for the 47.5MW Brockaghboy wind farm in Northern Ireland from ERG.

Its other vehicles are its £550m UK solar fund; and Greencoat Renewables, which it set up in early 2017 to invest in operating wind farms in the Republic of Ireland. This fund owns two wind farms totalling 137MW, but Nourse said he wanted Greencoat Renewables to reach the same size as its UK wind vehicle.

“We’ve moved from £260m in the UK in wind [raised at Greencoat UK wind’s initial public offering in 2013] to £1.5bn, and we want to do the same in Ireland,” he said.

2) …and is planning to grow outside the UK and Ireland.

Nourse also said Greencoat was looking to launch funds in other countries, including potentially the US and India. This could enable it to attract new types of investors.

He said:“Every year or so, we’ve found something different to do, and what we want to do is back management teams who come to us. We can go and talk to our investors that we’ve talked to, who’ve told us they didn’t like our current products, and say: ‘Would you be interested in this riskier product? This different product?’… I hope we might do dollars or rupees or something like that next, but truthfully we don’t know.”

3) He expects the UK to increase backing for onshore wind…

Nourse is also a non-executive director at nuclear group Urenco and sat on a panel that advised Dieter Helm on a UK government review into energy costs.

Nourse said he thinks there are ministers in the Department of Business, Energy & Industrial Strategy that want new auctions for established ‘pot one’ renewables technologies, including wind, and wanted to see if the Helm review could help make the case.

“When it’s so obvious [that established technologies offer LCOEs of] £20-£30/MWh, and you’re basically inflicting higher prices on the British energy customer, that’s an interesting position. I feel that will become unlocked in the next year,” he said.

Nourse said ministers might also be waiting to see if a pot one auction is needed, or if developers will find other ways to get financial certainty for their new projects – for example, power purchase agreements or other hedging mechanisms.

4) …but Brexit is delaying longer-term system planning.

Nourse was confident that the UK would continue to de-carbonise its energy system after leaving the European Union, because its plans are set by the Carbon Change Act rather than EU law. But he added that Brexit was delaying longer-term system plans.

He said: “I’m absolutely clear that they are starting to think about what the energy needs to look like if we move to 75% renewables, or we move towards 45% renewables and 40% nuclear… I fear that the thinking is not happening as fast as it should do.”

5) He isn’t attracted to investing in storage yet.

Finally, Nourse said he couldn’t yet see the case for Greencoat investing in storage as it is complex to explain to investors and doesn’t have a clear income stream.

“I’d love to have somebody come up and say: ‘You’re so ignorant and prejudiced… we can do this for you.’ If they did I’d say: ‘Brilliant, let’s go and find some investors. But I think it’s not yet infrastructure. The cashflows don’t feel infrastructure-like.”

You can hear more from experts like Richard Nourse at our conferences and other Quarterly Drinks evenings in London and New York.

For more details of upcoming conferences, click below...

Meanwhile, Russian trolls are fighting an aggressive social media campaign to try to shape the views of Americans about different power sources, and affect US energy policy. That’s the conclusion of a US House of Representatives report this month.

Naturally, both should be a concern for those investing in the US wind sector, and it may be tempting to see the first as the bigger issue. Undoubtedly, if hackers can disrupt the electricity system then that could hit production at wind farms, or cause blackouts in the whole grid, and have a significant impact on wind farm owners.

However, given all the discussion this week about the use of social media to influence elections, we’re more intrigued by the trolls.

The House of Representatives investigation says that the Kremlin-linked Internet Research Agency – a troll factory – put thousands of posts on Twitter, Facebook and Instagram from 2015 to 2017 in order to stir up controversy about US energy policy. The aim was to help Russia to achieve its geopolitical goals.

And this is where it gets interesting for wind investors. On one hand, the Russian government has been looking to these trolls to promote messages that support de-carbonisation, which includes talking up the potential of wind farms; and, on the other, it has been looking to ramp up the debate about climate change by showing it as a ‘liberal hoax’. Why take up these two conflicting positions?

Well, Russian foreign policy is never simple, but we'll give it a go.

In supporting de-carbonisation, the trolls were looking to make the case for ‘alternative’ sources, including wind and solar farms, in a bid to head off US support for shale gas fracking. This includes amplifying messages from green groups that it felt might be able to stop the use of fracking – and so keep the US reliant on Russia for fossil fuels. This may be beneficial for the wind industry but it still makes sense to be aware of who are friends and why.

Not that it worked. Since 2014, the US shale gas revolution has helped to drive down crude oil prices from over $100 a barrel to under $60, which has hit Russian energy interests. And the wind sector has also seen strong growth in the US since the extension of the production tax credit for the wind sector in late 2015. These are turning the US from a net energy importer into a net exporter.

Meanwhile, in spreading doubt about climate change, the trolls were seeking to sow discord in the debate about US energy policy; and breed public discontent in policies being pursued by political ‘elites', including fracking. It’s a familiar trope from recent UK and US elections, and this battle will continue. Despite the evidence, there will be an enduring debate about climate change and the extent to which human beings are responsible for it.

But there are steps that can be taken to protect energy investors. The US government is aware of Russian attempts to influence the energy market, and said it’s committed to running a market free from overseas interference. This doesn't mean the government can control the discussion, but at least it's aware of the threat.

The other good point for wind investors is that support for wind and other renewables is not just about climate change any more. The falling cost of wind power means the industry’s prospects are now tied far more to price and reliability than simply green concerns.

It won’t stop the Russian state-backed information war – but, for now, should give US wind operators some protection from it.

Wind Watch Who are you sending to Financing Wind New York? By Matt Rollason

Wind Watch is published every Monday, Thursday and Friday.

In the meantime, have you signed up for Financing Wind New Yorkon 30th May? All members are eligible to attend and, even if you can't be there, we'd love to host a colleague or client in your place. Make sure you're making the most of your membership...

We're hosting the event in association with our headline sponsor GCube Insurance Services and gold sponsor Marathon Capital; and we're looking forward to hearing from some of the top people in the North American wind market, with NYSERDA president and CEO Alicia Barton as our keynote speaker. She is set to talk us through the state's commitment to supporting large onshore wind and offshore wind projects; and what this means for businesses.

For more information on speakers and to download the agenda, take a look at the Financing Wind website.

Officials in US resort Ocean City are looking to push offshore wind farms further from the coast to protect tourism, but will it really help? Richard Heap reports

Officials in US resort Ocean City are looking to push offshore wind farms further from the coast to protect tourism, but will it really help?

Image credit: m01229 via Flickr

Four years ago, my family and I went on holiday to north Norfolk. The weather was pretty good for a holiday in England – and one of the highlights of that break was the time we spent in Sheringham, a traditional British seaside town. It had everything: the beach, the ice creams, the cheesy ‘wish you were here’ postcards.

And there was one thing we didn’t notice: the 317MW Sheringham Shoal wind farm, which was completed in 2012 and is located 11 miles offshore. Did it spoil anything? No. Hey, I even spend a few minutes poking around the visitor centre.

Maryland rejects new offshore wind

This is why I took great interest in a decision made by a committee of the Maryland House of Delegates.

Ocean City officials have claimed that the sight of wind turbines on the horizon would damage tourism, and force visitors to Jersey Shore or Virginia Beach instead.

There are two developments off the coast of Maryland that they’re worried about: US Wind is working on an up-to-250MW project 17 miles from the coast, and Deepwater Wind is working on its 120MW Skipjack 19.5 miles offshore. As you’d expect, the developers of both projects are opposing the officials’ arguments.

Arguments in favour of new offshore wind

Deepwater chief executive Jeff Grybowski also argued – correctly, in my opinion – that changing the rules for offshore wind now would scare away developers and investors. Maryland has fought hard to be supportive for offshore wind, and we don’t expect it to change now. It looks as though the officials in Ocean City will just have to get on with it.

Not that we think there’ll be much of a problem. For one thing, the turbines are so far offshore that we can’t imagine they’d cause a problem to anyone but the most ardent wind farm hater. Nobody’s proposing to erect them on the Ocean City boardwalk.

Sheringham Shoal didn’t cause a problem for me and my family – and evidently the number of offshore wind farms off the coast of north Norfolk isn’t causing problems for the tourism industry either. In 2012, tourism was worth £415m to north Norfolk according to consultant Destination Research, and this has risen to £434m in 2013, £470m in 2014 and £484m in 2015.

On that basis, it doesn't look like offshore wind has been putting people off.

But that’s just one example, so let’s also consider Brighton on the UK’s south coast, where E.On Climate & Renewables, Enbridge and a Macquarie-led group have been developing the 400MW Rampion eight miles from shore. Construction only finished last year and, so far, there's no evidence of a downturn in tourism.

Could wind farms be helpful to wildlife?

And closer to Maryland, there's Deepwater Wind's 30MW Block Island. Last month, the American Wind Energy Association and the Special Initiative on Offshore Wind released a video where Block Island residents talked about how the turbines were providing an ‘artificial reef’ that attracted fish, and recreational fishermen.

We can’t ignore that the video has a pro-wind agenda but, nevertheless, it makes an argument using local sources that offshore wind farms can actively help some parts of the tourism industry, and with little evidence that they do damage to others.

I haven’t been to Ocean City, but it looks like it has a wide range of attractions – more than Sheringham, anyway! In that context, the impact of a wind farm 17 miles from shore is, if you’ll forgive the pun, a drop in the ocean.

Each year, we discuss the biggest issues in European wind at our Financing Wind conference. Click below for details of upcoming events ....

Investors must take into account a large number of factors when deciding where to invest – but what about when the worst happens? Alice Jones looks at key risks

Investors must take into account a large number of factors when deciding where to invest – but what about when the worst happens? Alice Jones looks at key risks.

When deciding whether to invest in a wind farm, there are numerous considerations that companies must take into account – financial backing, legal requirements, local regulatory policy, calculating predicted revenue, and so on.

And as well as these considerations, there are also a host of other risks that can pose a threat to the profitability of projects. As the cost of wind power tumbles and project owners’ margins are squeezed, these risks could potentially be very damaging.

In this article, we outline the six biggest risks to your wind farm revenue – and what you can do to protect against them.

Anyone who read the news in 2017 did not have to look far for a natural catastrophe (‘nat cat’ to your insurers). During the summer, hurricanes Harvey, Irma and Maria wrought havoc across the US and Caribbean; Mexico suffered three earthquakes in September alone; and wildfires blazed across California during the autumn.

Meanwhile, Afghan avalanches, South Asian monsoon floods, and an earthquake on the Iraqi-Iranian border claimed hundreds of lives.

In addition to their devastating human impacts, the costs of natural catastrophes for renewables projects including wind farms is high – and countries that combine high ‘nat cat’ exposure with a high density of renewables projects are most vulnerable.

Reinsurer Swiss Re has estimated that, last year, these catastrophes cost the global insurance market $136bn – a significant proportion of which constitute losses to wind energy projects. Affected projects included a Puerto Rican wind farm that saw the blades snap off every turbine during Hurricane Maria, as well as solar PV projects that suffered smashed panels and destroyed electricity cables.

With expert meteorologists such as Aeris Weather predicting that climate change-caused volatile weather patterns are set to increase, ‘nat cat’ is poised to become a progressively greater threat to wind farm revenue in the coming years, with monetary losses stemming not only from the cost of replacement parts and technicians’ time, but also from loss of revenue while a project is ‘offline’ (‘business interruption’, or BI, costs).

Carefully completed due diligence offers the best means of protection, and investors will need to decide whether the opportunity of higher returns in emerging markets is worth the higher ‘nat cat’ risks that characterise some of those countries.

2) MECHANICAL AND ELECTRICAL BREAKDOWN

Like any machinery, wind turbines are susceptible to the odd malfunction – with three of the most common manifestations being blade failure, gearbox failure and fires, as reported by GCube Insurance.

In the past, issues have often been traced back to serial defects in certain turbine models, which have then been rectified and replaced under original equipment manufacturer (OEM) guidelines.

Other common causes of breakdown have been identified as strong gusts of wind that cause blade over-speed and excessive loads, lightning damage, human error, and electrical issues often attributable to excess voltage or current leakage.

As the wind industry continues to scale up both in size – with GE announcing plans for its 12MW Haliade-X turbine platform in March 2018 – and ambition, the potential risks rise too. Not only do larger turbines account for a greater proportion of project revenue – so having a greater impact if they break – than a series of smaller ones, but risks are also introduced by supply chains which lack experience in dealing with much larger turbine blades and other equipment.

Meanwhile, new technologies – such as floating wind – require developers and OEMs to apply methodologies developed on more traditional projects to new ventures, in a necessary but imperfect transition period which inevitably increases risk.

In the face of these risks, OEMs will continue to find new ways to cope. This will include the use of predictive analytics and condition monitoring systems to forecast when failures might happen; and the use of failsafe technology to minimise damage when disaster strikes.

Due to their sporadic and variable nature, such mechanical and electrical breakdowns will remain difficult to predict – but choosing OEMs carefully, and ensuring that turbines are maintained correctly, will go a long way towards minimising risks.

3) POLITICAL AND REGULATORY RISKS

Political risks naturally pose the greatest threat to those projects located in countries with volatile political climates, many of which are also in wind’s emerging markets.

This political risk map from Marsh is not specific to the wind sector, but it provides a good overview of current global risk levels. Latin America, Africa and the Middle East are all examples of areas in which rapid investment in wind farms – often prompted by government targets, such as Egypt’s ambitious goal to provide 12% of its energy from wind by 2022 – means that more investors will be exposed to political risks.

These risks can come in many forms, and damage to projects is often virtual, rather than physical, with CEND (confiscation, expropriation, nationalisation and deprivation of projects) posing the greatest threat. And they aren’t the sole preserve of emerging markets – for example, last year we saw the US developer Invenergy LLC sue the Polish government for a claimed $700m loss from wind farms in the country, citing actions ‘tantamount to an expropriation’.

And some wind farms have been physically damaged, either deliberately caused by, or as a by-product of, riots, violence and even acts of terrorism.

Meanwhile, a number of recent regulatory changes in Europe and the US threaten the stability of project revenue in established markets. The French government’s attempt to retroactively renegotiate offshore wind subsidies, and the potential impact of President Trump’s tax reforms, offer just two examples.

Investors can use resources such as Marsh’s political risk map to inform decisions about project sites – but the risks remain difficult to predict and, particularly in those countries with high risk factors, investing in political risk transfer mechanisms and insurance will often be necessary to ensure security of revenue.

4) LOCATION RISK

Location risk is, to some extent, linked to political risk and is also at its highest in emerging wind energy markets. A lack of applicable supply chain experience and established infrastructure, as well as a shortage of skilled personnel, can make emerging markets some of the riskiest locations in which to build a wind farm – despite the attractive opportunities offered by cheap land and strong winds.

This can be compounded by local hostility to projects, which can threaten physical destruction and legal contentions to wind farms. For example, we reported in early 2017 on a landmark Thai Supreme Administrative Court ruling that pronounced plans for a wind farm on ‘sor por kor’ land, which is designated for agricultural uses only, to be unlawful and suspended permission for the projects to be developed.

Risk levels can also be influenced by the precise physical location of the wind farm site; particularly its distance from cities, from skilled workers and not least, from the OEM – or, if parts are shipped from overseas, from relevant shipping ports.

Expensive and sensitive pieces of turbine equipment such as the nacelle do not take well to being transported in inadequate vehicles, or on basic roads. In the past, this has led to cases in which equipment has been purchased and transported to the remote location chosen for the wind farm, only to arrive damaged. The cost of acquiring and transporting replacements is then compounded by project delays and BI costs, constituting a significant knock to profitability.

This risk remains as long as the wind farm is operational: the further the wind farm is from manufacturing facilities and skilled technicians, the longer it takes to repair and bring turbines ‘online’ again if they are damaged during their operational lives.

In addition to choosing your wind farm site carefully, and particularly when building in emerging markets, the importance of implementing corporate social responsibility (CSR) principles can’t be overstated. Hiring local workers, maintaining transparency and remaining aware of local legal frameworks will all help to prevent losses caused by legal challenges to a wind farm – or even the physical destruction of it.

5) WEATHER RISK

On the opposite end of the scale to natural catastrophe, weather risk refers to the loss of revenue that occurs when, put simply, the wind just doesn’t blow.

With climate change causing increasingly-unpredictable phenomena, in recent years we’ve seen wind speeds drop in key markets such as northern Germany. Meanwhile, many US firms cited low wind speeds as a major reason for profit dips in 2017.

The first line of defence against this risk is to invest heavily in weather data before choosing a wind farm site. Weather measurement firms can provide comprehensive data as to recent, and predicted future, wind speeds by geographic location. This is useful not only for deciding on a site but also for calculating predicted revenue and securing financial backing.

A geographically-diverse wind portfolio can also offer some protection: wind speeds are unlikely to dip in both Chile and Thailand at the same time, for instance. New risk transfer and insurance mechanisms can also offer financial security.

6) CYBERSECURITY RISK

In recent years, we’ve seen cyberattacks become a significant threat to technology-driven sectors – and any business that uses computers. As renewables networks and grids become more interconnected, the threat level to wind farms is rising too.

Costly cyberattacks could come in many forms, from the manipulation of turbine blades to minimise efficiency, to total paralysis of the system. With modern wind farms often being controlled from afar, weak points in online control systems are leaving projects increasingly vulnerable to attack.

Researchers presenting at the 2017 Black Hat cyber security conference in Las Vegas also revealed deficiencies in wind farm security measures, as the Financial Times reported from the conference. A lack of message encryption, and the joined-up nature of turbine networks – meaning that a hacker could use one turbine as an access point for the entire farm – were cited as major vulnerabilities.

While cyber risk is a relatively new and undocumented threat, hackers appear to attack wind farms for one of two reasons: either to seek ransom payments in return for the restoration of operations, or for non-monetary reasons such as an ideological or political protest. We could well imagine Russian hackers seeking to undermine the reputation of renewables as an alternative to fossil fuels, for example.

A report by the Renewables Consulting Group and Cylance Inc., ‘Cybersecurity in renewable energy infrastructure’, analyses cyber risk to renewables projects and offers specific suggestions for revenue protection. This includes investing in security measures, as well as developing an emergency plan for if the worst should happen.

CONCLUSION

The wind market is growing in scale and ambition across the globe. However, with expansion and innovation comes risk and, as the opportunities in the wind sector increase, so do the threats to projects and to the revenue they provide.

Costs can be immediate – the price of replacing parts and paying for technicians’ time – and compounded by ‘hidden costs’ from hiked insurance premiums and BI costs. This could be devastating for firms who are working with slim margins.

Nonetheless, awareness is the first step to prevention. With proper due diligence and back-up insurance protection, there is no reason why a wind farm shouldn’t survive – and thrive – despite these risks.

Each year, we host conferences discussing the biggest issues in European and North American wind. For more details, click below...

Maybe it was the Guinness talking. At a St. Patrick’s Day lunch in Washington DC on Thursday, Irish Prime Minister Leo Varadkar boasted about how he got involved in the planning process for a wind farm in 2014 at the behest of the not-yet-president Donald Trump. Well, I guess it's nice to hear a politician telling the truth.

And just in time for the Irish Wind Energy Association’s annual spring conference in Dublin this Wednesday and Thursday. The political climate for the wind market in the Republic of Ireland was always going to be a big talking point at the event, but we’re sure Varadkar’s bout of braggadocio will add spice to the discussion.

The story dates back to 2014. Varadkar was Irish tourism minister and Trump was a brash billionaire who was investing in two golf resorts in the UK and Ireland.

Trump had already spent a few years in dispute over plans for a Vattenfall wind farm off the coast of Aberdeen Bay, which he said would spoil views from his Trump International golf resort in Scotland. He lobbied Scotland’s then-first minister, Alex Salmond, and other British politicians to have the development cancelled.

Unfortunately for Trump, Salmond showed a bit of backbone and the billionaire had to pursue his case through the courts – where, again, he lost. Hmmm... I thought Donald Trump always won.

And so, when Trump heard about a similar wind farm that Clare Coastal Wind Power was planning near his Doonbeg golf resort in 2014, he used similar tactics.

Varadkar said at the lunch that Trump called him to say he was concerned that the project would damage Doonbeg’s landscape and affect his resort. Varadkar said he then “endeavoured to do” what he could, and talked to Clare County Council about the planned wind farm. The council ultimately refused the scheme.

“The president has very kindly given me credit for that but it would probably have been declined anyway,” he said.

Varadkar’s spokesman has since downplayed the intervention, and that he simply “sought clarity from the local authority”.

In addition, a representative from County Clare said that Varadkar did not seek to influence the decision, and the inquiry was made from his office in the form of a ‘status update’: “Effectively, what [Varadkar] did was sought information,” said the representative.

Not that this denial is worth much to opposition politicians or the developer in question. Labour leader Brendan Howlin called it “extraordinary” and “entirely inappropriate” for the now-prime minister to “meddle and intervene” with planning; and Michael Clohessy, director of Clare Coastal Wind Power, said the firm was “disappointed at the admission… that he interfered in the planning process”, and was now reviewing its options.

Whatever happened in this case, it puts a spotlight on the fairness of the system for supporting and approving wind farms in Ireland.

The system is currently in a state of flux, as the industry is waiting for the final version of the new Renewable Energy Support Scheme, which is set to introduce auctions from 2019; for the launch in May of the integrated single electricity market for the island of Ireland; changes to grid access rules; and changes to the rules for planning consent in the ‘Wind Energy Development Guidelines’. These are four huge areas that could all have a big impact on the system individually, and all are crucial for investors.

Ken Boyne, managing director at Ionic Consulting, said that the industry is waiting for clarity in all of these areas, and there was a risk that too many changes were being made at once.

However, he added that the positive take was that it could lead to the government to introducing a coordinated approach that would help the wind sector. Investors will definitely be hoping so.

And, with Varadkar’s statement last week, the need for clear and transparent rules will be more important than ever.

To re-cap, longstanding rivals E.On and RWE have agreed a complex €60bn asset swap that is poised to turn E.On into a company focused purely on networks and retail customers, and establish RWE as Europe’s third-largest renewables group.

Here are the details of the agreement.

E.On is set to buy a 76.8% stake in Innogy, RWE’s renewable energy subsidiary, including its grid & infrastructure and retail businesses. This is valued at €43bn.

Simultaneously, RWE is set receive a 16.67% equity interest in E.On, including its renewables business, and pay E.On €1.5bn in cash. RWE is also poised to keep Innogy’s renewables assets; its gas-storage business; and its stake in Austrian supplier Kelag. The assets handed over to RWE have been valued at €17bn.

And E.On could make a public takeover offer in cash to the shareholders of Innogy at €40 per share, which would value the remaining 23% at around €5bn.

The deal still requires approval from regulatory and competition authorities, who we are sure will look at the plan very closely. It is due to complete by the end of 2019.

We have been aware for many months about speculation over Innogy’s future but, even so, a tie-up between these two great rivals is a blockbuster story. And it is a story that has its roots in Germany’s energiewende. This is the country’s move to embrace renewable energy sources that became law in late 2010.

Germany's decision to focus on expanding wind and solar power has put pressure on the two groups’ core conventional power operations – and therefore their financial results. The companies reacted in similar ways.

In 2016, E.On spun off its conventional power operations into new subsidiary Uniper, keeping renewables, networks and customer solutions. And, in the same year, RWE spun off its renewables, retail, grid and infrastructure businesses into Innogy, while keeping its legacy coal business in RWE.

Despite this, both groups reported losses in 2016 and have been looking for ways to boost their fortunes. This led to E.On agreeing to sell 47% of Uniper to Finland’s Fortum in a deal that is yet to complete, and RWE looking at options for its 76.8% Innogy stake. That is how we’ve ended up with this €60bn transaction.

This deal is set to make E.On Europe’s largest network and energy retail group, with a regulated asset base of around €37bn; while RWE will end up as Europe’s third-largest renewables player, after Spain’s Iberdrola and Italy’s Enel, with a renewables portfolio of over 9GW. This would be made up of E.On Climate & Renewables’ 5.3GW wind and solar portfolio, and Innogy’s 3.9GW.

Specifically, wind would be a very large part of the green RWE’s portfolio. It would own 5.3GW of onshore wind farms and almost 2GW offshore, and with plenty of growth potential. Innogy has recently bought EverPower’s 2GW US wind portfolio, and taken full control of a 1.2GW project in the Dogger Bank zone and the 860MW Triton Knoll.

Not that everyone has been impressed with Innogy’s expansion plans. The clearest example is the exit of chief executive Peter Terium in December following concerns from investors that he had lost focus on profits in favour of overseas growth. Indeed, net profit fell from €1.6bn in 2016 to €908m in 2017, according to the annual results that it published this week. In that context, the opportunity to merge Innogy with the apparently more conservative E.On Climate & Renewables looks like a smart move.

But it won’t be simple, and there will be pain. E.On said it would look for up to €800m cost savings in both companies following the deal, including up to 5,000 job cuts. We don’t expect renewables to be the focus of these cuts, but they won’t be exempt.

There's also a long way to go before the deal concludes, but it looks set to overhaul the business models of both firms. The pair of them were arguably too slow to adapt to the energiewende – and this could just be the solution they were looking for.

For the latest in our series of member Q&As, we spoke to Julien Sellier of Structeam Ltd.

For the latest in our series of member Q&As, Frances Salter spoke to Julien Sellier of Structeam Ltd. If you'd like to take part in a member Q&A, email us at editorial@awordaboutwind.com.

Julien has been involved with designing and manufacturing wind turbine blades since 2004. In 2010, STRUCTeam was founded to support the wind industry through reducing risk and costs. Julien is the Managing Director of STRUCTeam and consults for key clients with respect to their long term blade strategy, in terms of technology and supply both for onshore and offshore wind.

In the simplest terms, what does your company do?

We are consultants in blade technology, as well as being contractors. This means we are specialists in advanced materials such as fibre re-enforced plastics and the technology used to make blades cost-effectively. We work in Europe, India and China.

Of the deals you’ve worked on, which is your favourite and why?

I have many favourites: one would be when we got our first blade design in 2011, which was certified through DNV-GL. The main achievement was to convince this first customer that we would deliver with our newly formed company, and we delivered; that’s why it was is so symbolic for the company.

In which markets do you see the biggest opportunities right now?

Probably China has the lion’s share, but Europe and America are also significant.

What do you think is the biggest challenge facing the wind industry, and how would you solve it?

I think it’s operations and maintenance because the investment phase is now well understood. The little operations and maintenance problems become bigger as the industry grows. We have to remember that 10 years ago, 2MW turbines were the largest platform available: now it is in the region of 6-8MW. This scalability comes with consequences and has an impact on the supply chain, which needs to become more proficient and organised. With the work we do, we are basically de-risking the future activities of our customers.

Which trends do you think will affect the wind sector the most in the next 5-10 years?