O-O-O-O-Oklahoma, where the wind farms spin upon the plain,

And lawmakers gas but do not pass,

a tax bill to stop credits again.

O-O-O-O-Oklahoma, ev’ry night Invenergy and friends,

Go to bed and think: ‘Will the state sink,

our plan before the PTC ends?’

When I win the contract to re-write ‘Oklahoma!’ – hey Rodgers & Hammerstein estate, call me – I’ll make it about wind farms. The state’s approach to wind is as dramatic as any Broadway musical.

This week, the state Senate voted against a plan to end a lucrative tax credit for the wind sector. Under current rules, project owners earn ‘zero-emission tax credits’ that they can redeem to cut their state tax bills. This was introduced in 2003 to support the fledgling wind industry. It was ruled out for new projects from last July.

However, this week the Senate rejected a plan to take these cuts further and retroactively change the rules for working wind farms.

Some in state government wanted to cut these tax benefits to save $500m over ten years to plug an $870m hole in the state budget. It was rejected, rightly in our view. This would have done huge harm to the business models of wind farm owners in Oklahoma; to the confidence of investors; and would have led to legal action too.

This is significant for the wind industry as it gives a taste of battles yet to come. Yes, the business case of wind is getting stronger, as the cost of producing electricity from wind farms falls.

But the upshot is that states will look at whether incentives they are giving the wind industry are too much. We’ve seen retroactive changes in countries like Spain with disastrous results, and we’ll surely see it at state level too. In fact, it’s often the most generous governments that then have to act the toughest. This is because generosity attracts business – but can require bigger cuts later.

In the case of Oklahoma, this also creates difficulties for one of the country’s biggest wind projects: Invenergy and American Electric Power’s $4.5bn 2GW Wind Catcher.

The companies are hoping to win final backing by the end of June, which is key if they are to complete it in 2020 to win full backing from the wind production tax credit. They also need to secure regulatory backing in Arkansas, Louisiana and Texas.

But Wind Catcher has been held up by the thorny question of ‘cost recovery’ by the developers in Oklahoma. Invenergy and AEP say that consumers should foot the bill for the $4.5bn development because it would generate greater savings than that for the public, but a judge ruled against them in February. AEP has been working hard to win backing from various groups but the regulators are key.

No doubt it’ll be a big talking point at AWEA Windpower next week.

There will probably only be a limited amount we can read into the final decision at Wind Catcher when it comes out.

This is the largest single-site wind farm planned in the US, and so there is a sense in which any decision here is exceptional and a one-off. But it will indicate how favourable Oklahoma is likely to be for wind investors in future, and how tough states will be when it comes to offering support to wind firms.

And this is the challenge for investors in the coming years.

In states like Oklahoma, it is well-established that wind farms can bring financial benefits; and that this sector is a serious competitor to the oil and gas industries. But investors have to keep making the point that the sector still needs political backing, even if this doesn’t take the form of new financial subsidies; and that wind developers will only continue to be active in states that don’t change the rules of the game during the lifespan of their schemes.

Good sense has prevailed in Oklahoma once this month, but we'll see other states look to retroactively change support mechanisms; and, when we do, the industry must be ready to fight its corner.

Not a sexy message – it's hardly the stuff of a rollicking Broadway number – but important nonetheless.

Article search

Wind Watch

Who are the top lawyers in the wind industry?

By Richard Heap

On 14th August, we are due to publish the second edition of ourLegal Power List and we need your help.

This is our 'who's who' of the most influential lawyers operating globally on the biggest deals in wind energy, including major transactions, mergers and complex project finance deals.

The idea is to recognise those who keep the financial side of the industry moving smoothly, often from behind the scenes.

This is your chance to nominate those lawyers who you feel have shown exceptional professionalism and dedication within the last year or so -- or, indeed, to nominate yourself! This includes in-house lawyers and those at law firms.

What we need from you is:

- The name, company and job title of your nominee

- A short description of the deals they've worked on

- A brief explanation of why we should include them

Please keep this to 250 words or less and email your preferred nominee at editorial@awordaboutwind.com. We'll be closing nominations on 8th June: if you don't tell us by then, you could miss out. We'd love to read your nominations.

In our Finance Quarterly Q2 2018 report, we delved into our deals database to bring you the latest deals from around the world. This includes information on the most significant project M&A, project finance, corporate M&A and power purchase deals between January and March.

In our Finance Quarterly Q2 2018 report, we delved into our deals database to bring you the latest deals from around the world. This includes information on the most significant project M&A, project finance, corporate M&A and power purchase deals between January and March.

Here we have highlighted the five most interesting offshore project M&A deals, which have been reported in the first quarter of 2018.

1) Equinor enters Polish offshore wind market

Norwegian oil firm Equinor (formerly Statoil) entered into an agreement in March to acquire a 50% interest in two early-stage offshore wind projects totalling 1.2GW in the Polish Baltic Sea, from Polenergia. This deal has made Equinor the first foreign company to bet on the success of the Polish offshore wind sector.

Poland is taking steps to install 4GW of offshore capacity by 2030, and state-owned transmission system operator PSE has recently said that this potential capacity could double to 8GW, if the government carries out network upgrades. Polish utility PGE is also looking to develop up-to-2.5GW of offshore wind farms off the Polish coast.

Find out more about offshore wind in Poland here.

2) Mitsubishi buys into Moray East

A subsidiary of Japanese conglomerate Mitsubishi last month bought a 33.4% stake of the 950MW Moray East in UK waters.

Big Japanese corporations have continued to show interest in the European offshore market as slow growth of the sector in their home market, falling costs and Japanese interest rates at a record low of -0.1% have pushed them to look at offshore wind investments in Europe for long-term returns. Mitsubishi is also reportedly looking to invest in the 370MW Norther off the Belgian coast and the 130MW Luchterduinen off the Dutch coast.

Members can read more about the Japanese wind market here.

3) Innogy invests in offshore wind in Ireland

German utility Innogy last month bought a 50% stake of the 600MW Dublin Array offshore scheme in the Irish Sea from local developer Saorgus Energy.

This deal is part of a growing interest that companies have been showing in the Irish offshore wind sector. This includes Belgian developer Parkwind becoming a strategic partner in the planned 330MW Oriel offshore wind farm last October and Element Power acquiring the 750MW North Irish Sea Array from Gaelectric last week.

Since the Irish government excluded offshore wind from renewable energy support schemes in the mid-2000s, the sector has stalled. However, the new Renewable Energy Support Scheme together with the rekindled interest of investors is set to give a new start to the Irish offshore wind market.

Find out more in this blog post by Ionic Consulting’s Ken Boyne.

4) Shell-led consortium sells stake in Borssele 3 & 4

Anglo-Dutch oil giant Shell and its partners Eneco and Mitsubishi sold in January a 45% stake of the planned 731MW Borssele 3 and 4 offshore development to investment manager Partners Group. The consortium, which also includes Van Oord, won backing in December 2016 to develop Borssele 3 and 4 at a strike price of €54.50/MWh in waters off the Netherlands.

The move is set to allow the companies to scale back financial exposure to the wind farms and recycle the cash in new projects. In particular, this fits into the strategy recently announced by Shell, to invest up to $6bn via its new energies arm by 2020 in sectors including wind and solar.

5) ESB enters offshore wind with Galloper deal

Irish state-owned utility ESB bought last month a 12.5% stake in the 353MW Galloper wind farm in UK waters from Macquarie Capital.

This means that ESB has joined Innogy, Macquarie’s Green Investment Group, Siemens Financial Services and Sumitomo Corporation as partner in the £1.5bn project. The deal represents the first investment by ESB into the offshore wind market and is part of its strategy to develop and acquire offshore wind farms totalling up to 1GW off the UK and Ireland by 2020. Galloper was fully commissioned at the end of March.

Seabirds change their flight path to avoid collisions with offshore wind turbines. That sounds like good sense from our feathered friends but, for the developers of these projects, it is a big deal.

This month, the Offshore Renewables Joint Industry Programme published its 248-page Bird Collision Avoidance Study, which analyses seabird behaviour and collision risk at offshore wind farms. The study was commissioned by 11 offshore wind farm developers including Swedish utility Vattenfall; managed by UK organisation Carbon Trust; and backed by the UK government.

The study analysed seabird activity for two years at Vattenfall’s 300MW Thanet wind farm in UK waters. Its analysis was carried out by human observers and a system that automatically records seabirds’ movements. This resulted in a massive data collection, including over 600,000 videos.

Of these, around 12,000 videos contained evidence of bird activity – but only six collisions with turbines were observed. This is less than half of what the researchers expected and is the result of seabirds change their flight path to avoid being hit.

Talking to A Word About Wind, Carbon Trust director Jan Matthiesen said that this is relevant for investors because it shows, for the first time, evidence of the behaviour of birds approaching offshore wind farms: “We have actually seen that seabirds are consciously avoiding the turbines, as they now have a much better understanding of the movements of the turbines. This has never been seen in this way before.”

The study shows that seabirds have adapted to the presence of wind turbines in the sea. He said: “When you cross the road, you know that you have to avoid the cars, because you have learned as a child that they represent a danger. Birds have been learning in the same way how to behave in presence of turbine blades.”

The study’s findings are particularly relevant for offshore wind developers, as the risk to seabirds has heavily affected the progress of schemes. The most famous example is the four-year legal battle led by wildlife charity RSPB against four offshore wind projects totalling 2.3GW in Scottish waters. Its case, that Scottish ministers had not properly considered the impact of this quartet on seabirds, was dismissed by the Supreme Court last November.

Matthiesen says the study would help developers in two ways.

First, he said evidence of seabirds’ avoidance behaviour would reduce consenting risk. The consenting process of offshore wind farms requires identification, prediction and evaluation of the environmental effects of the proposed projects; and the risk of birds colliding with blades is one of the most significant environmental impacts. This evidence of the birds’ behaviour could speed up the permitting process, providing a more realistic and reliable evaluation of birds’ collision risk.

Second, Matthiesen argued that the extensive dataset of observations of seabird behaviour collected by the study would enable developers to update their collision risk models.

Collision risk models currently used by offshore wind developers are often based on data from onshore wind farms, for example. This is not ideal because it is based on different turbine designs in a different landscape where birds may behave differently.

They also predict the number of collisions based on linear flight patterns, assuming that birds take no avoiding action. The data collected by the study can now be used to update these models, to show a more accurate collision risk. This is crucial at a time when the next generation of wind turbines are developed.

However, the study has some limitations: it currently relies on data collected at one site only, largely during daylight and good weather conditions, so may not capture all the variability in relation to weather, visibility and regional differences. Matthiesen said there is scope to extend the research and make it more comprehensive.

Even so, studies like this make a valuable contribution to growth of the offshore wind sector, as they help developers and investors to ease fears that wind turbines harm wildlife. And that’s a goal that most in the sector and those outside it can agree on.

This month, Germany concluded its first joint tender for wind and solar power. The result wasn’t pretty for wind. Solar developers won all the 200MW capacity on offer, and even the head of the German solar association said that wasn’t a healthy situation.

The paucity of orders from this auction will further ratchet up pressure on Germany’s wind turbine manufacturers, who are already struggling to cope with low margins as a result of the tumbling cost of wind energy in recent auctions.

A government move to reduce annual installations to 2.8GW and the dominance of citizens’ groups, who may not need turbines for many years, in the first tenders last year don’t help either.

This would be well down from the 6.6GW installed in Germany last year – 12% of the global market – and is forcing manufacturers to make tough decisions on jobs. Siemens Gamesa announced 6,000 potential redundancies last November, while Enercon, Nordex and Senvion have set out their own restructuring plans. This might be necessary for the wind industry to adjust to lower prices, but let’s not forget the human cost.

These pressures are also pushing manufacturers to overhaul their operations. For example, Senvion has merged its operational hubs in the central European Union and northern European Union into a new ‘EU North hub’, so it can consolidate its operations in the two markets and concentrate more of its efforts on emerging markets.

The combined hub is headed by Jochen Magerfleisch, Senvion’s EVP for sales in Europe; and is part of the firm's ‘Move Forward’ programme launched two years ago.

He told A Word About Wind there would still be activity in core European markets – notably Germany, Ireland, Norway, Sweden and the UK – but that Senvion planned to focus on opening new European markets too, including Lithuania, Estonia and Latvia. They're not big but they could help it cope with less in Germany.

“The dependence on the European core market is a danger for companies, as all German manufacturers are. We’ve been able to reduce our dependence on these markets,” he said.

Outside Europe, Senvion is also focused on growth in the South American market including Argentina and Chile; in Asian countries including India, Japan and South Korea; and Australia, where the market picked up again last year.

Magerfleisch said that while competitive tenders are driving down the cost of wind energy in established markets, there is a limit to how low they can go: the average price on the spot market. This means that, if wind farms can deliver wind energy at a cost of €35/MWh-€37/MWh, the pressure on turbine makers would fall.

Pressure in Europe has also forced German manufacturers to look at mergers and acquisitions with emerging markets specialists: the tie-up of Siemens and Gamesa is the biggest recent example, and follows the €785m buyout by Nordex of Acciona’s wind operations. In these cases, the argument was that bigger was better.

Magerfleisch disagrees with that logic. He said there's a benefit to some firms being smaller, as it means they can make quicker decisions to move into new markets and change their strategy: “It’s not a question of size. It’s a question of speed,” he said. “It’s not a given that some smaller players are not able to survive.”

He said Senvion has a 5GW-6GW addressable market – the market it can serve with its current machines – and it should be able to maintain a 10% market share in the coming years. In total, the company sold 1.48GW of turbines in 2017, which is below the 1.76GW in 2016 and 1.75GW in 2015, but back to a 2014 level.

The company is still focused on further developing its platforms to work in cold climates and is looking to develop its offshore turbines for use from around 2022. In addition, Senvion continues to grow its service offer to support existing customers.

There will continue to be pressure for German manufacturers in 2019 and 2020, and this will lead to more tough decisions for the companies and their employees. But for some, ‘agility’ rather than ‘acquisitions’ look like being the ‘A’ in their business alphabet.

Now I’ve written that, they’ll probably buy someone next week!

Wind Watch

How can wind turbine makers use their product portfolios to boost profit margins?

By Philip Totaro, Founder & CEO, Totaro & Associates

With more than 7GW added in 2017, the United States wind energy market is seeing robust growth. Vestas has maintained its leadership position in annual capacity additions with 2.5GW, while General Electric stays a close second at 2GW. Siemens Gamesa Renewable Energy had a noteworthy uptick in capacity additions to 1.6GW and Nordex / Acciona comes in fourth at 0.8GW.

But digging deeper for the reasons why Vestas, GE and SGRE have largely dominated the US wind energy market unveils some clear patterns and surprising trends. A key factor that has enabled the success of these three OEMs is the diversity of their product portfolio to serve almost any power density. Nevertheless, GE and SGRE have struggled with profitability, so why isn’t the increased sales volume translating?

The answer is return on capital. With so many in the industry focused on reducing the levelized cost of energy across their product portfolio, they have failed to implement their product strategy in a way that maximizes global product sales for a specific turbine model to offset the capital expenditure investment required in the development of that model.

A contributing factor to this poor return on capital, as well as the significant amount of under-exploitation of some wind regimes in the US market, stems from historical patterns in product development and capacity build-out by developers.

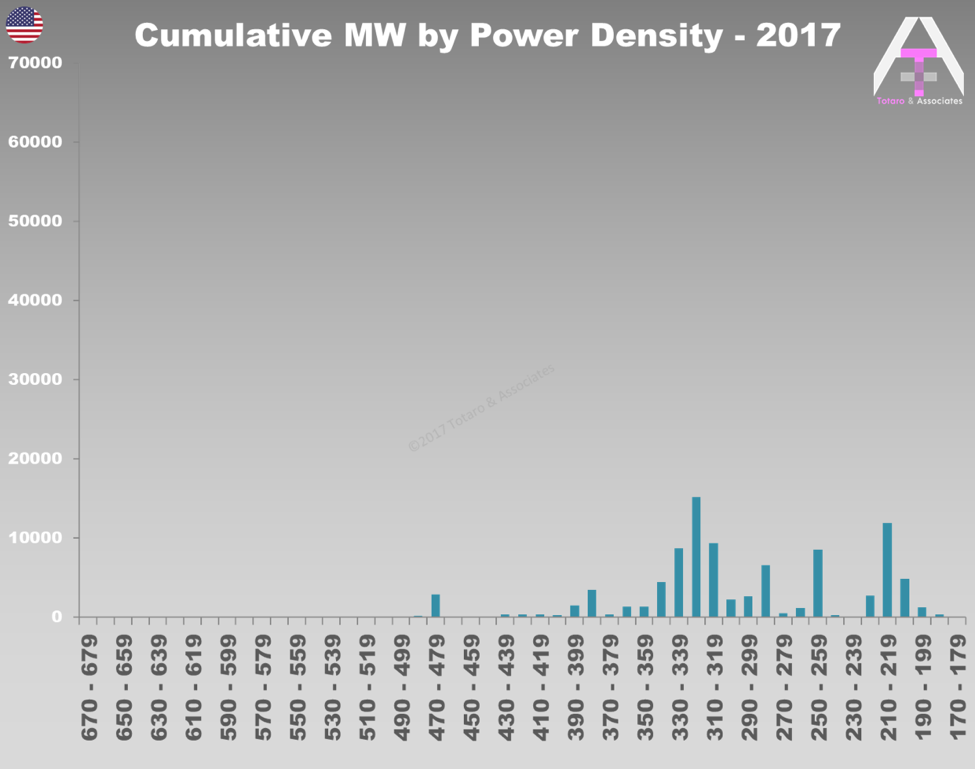

When evaluating the market based on power density of the turbines (i.e. power rating of turbine / swept area of rotor), we see an interesting trend emerge, where capacity additions are largely concentrated around turbines with standard IEC [International Electrotechnical Commission] wind class distribution (see graph 1).

But when the market resource potential is overlaid on this installed base distribution, another interesting trend emerges (see graph 2).

Guest blogger Philip Totaro - founder and CEO of Totaro & Associates - shares his thoughts on how firms can develop their project portfolios to improve their profit margins.

Guest blogger Philip Totaro - founder and CEO of Totaro & Associates - shares his thoughts on how firms can develop their project portfolios to improve their profit margins.

With more than 7GW added in 2017, the United States wind energy market is seeing robust growth. Vestas has maintained its leadership position in annual capacity additions with 2.5GW, while General Electric stays a close second at 2GW. Siemens Gamesa Renewable Energy had a noteworthy uptick in capacity additions to 1.6GW and Nordex / Acciona comes in fourth at 0.8GW.

But digging deeper for the reasons why Vestas, GE and SGRE have largely dominated the US wind energy market unveils some clear patterns and surprising trends. A key factor that has enabled the success of these three OEMs [original equipment manufacturers] is the diversity of their product portfolio to serve almost any power density. Nevertheless, GE and SGRE have struggled with profitability, so why isn’t the increased sales volume translating?

The answer is return on capital. With so many in the industry focused on reducing the levelized cost of energy across their product portfolio, they have failed to implement their product strategy in a way that maximizes global product sales for a specific turbine model to offset the capital expenditure investment required in the development of that model.

A contributing factor to this poor return on capital, as well as the significant amount of under-exploitation of some wind regimes in the US market, stems from historical patterns in product development and capacity build-out by developers.

When evaluating the market based on power density of the turbines (i.e. power rating of turbine / swept area of rotor), we see an interesting trend emerge, where capacity additions are largely concentrated around turbines with standard IEC [International Electrotechnical Commission] wind class distribution (see graph 1, below).

But when the market resource potential is overlaid on this installed base distribution, another interesting trend emerges (see graph 2, below).

Specific segments of the market are seeing saturation with multiple OEMs competing fiercely for market share with overlapping turbines in the same power density range. In other market segments, such as a power density range of 230 - 239 W/m2, the US market is seeing little to no capacity penetration whatsoever up through 2017.

The reason for this is that project developers have historically favoured the wind regimes with the best proximity to transmission as well as the availability and scale of turbines, which were aligned with IEC wind class sites. This has ensured maximum payback on project sites in the past, but it has left a significant portion of the US wind resource to see little deployment (see graph 3, below).

While the product portfolios of the top three OEMs in the US have centered around standard IEC wind class products, GE, SGRE and Vestas have also seen a broader diversity of sales thanks to ancillary products that lie in between conventional wind classes.

As a result, some OEMs have taken note of this development pattern, and created a robust product portfolio that can be offered in any market segment regionally and globally. Combined with modular turbine technology architecture, they are seeing better production economies of scale with their product portfolios.

But will that answer the return on capital question? Not entirely. To see this, let’s look at the mapping of the Vestas product portfolio to the US market vs. a smaller competitor like Suzlon.

Overlaying the Vestas product portfolio on the US market resource map highlights this trend towards greater product portfolio diversity. Vestas has developed a ‘product for all seasons’ strategy with a wind turbine in either the 2.X, 3.X or 4.X MW range to serve almost the entire US market (see graph 4, below).

By contrast, Suzlon has a product portfolio that has some potential to capture additional market share, but they have not focused on development of products to capture share in traditional IEC wind class ranges. This is a result of bringing a product designed for the market in India to the US and hoping it will sell, rather than a dedicated product portfolio that has global appeal and diversity, like Vestas (see graph 6, below).

Looking at GE and SGRE, they have product portfolios that are strikingly similar to Vestas with a comparable level of diversity, but with one exception, less profitability on their sales. Why?

Since 2011, Vestas has developed a product portfolio based on product families, rather than a diverse array of individual wind turbines serving individual regional markets. These product families share the same rotor, a similar gearbox, a similar or the same generator, the same tower internals, etc. in an effort to minimize variation throughout the product portfolio and drive supply chain efficiencies with scale.

Additionally, blade capex investment per turbine model can be justified due to wider market specific sales or global sales through export from a primary market versus the development of a market specific turbine in every region of the world.

GE and SGRE also have a wide array of products, but their return on capital has been far less than Vestas due to a later adoption of the modular platform architecture. GE currently has 15 different rotor sizes for turbine nameplate power ratings of 1.7 – 4.8MW.

With capex investment per turbine model of each family between US$30m–$80m, this implies there is a minimum threshold of product sales for each turbine model for which that capex investment breaks even. On some products, GE has not seen the production volumes necessary to break even, while on others they have. In aggregate, sales across the product portfolio have not equaled the capex investment associated with such a diverse product range.

One reason for this is the cannibalization of turbine sales for models that serve the same segment of the market, such as the GE 1.79-100, 2.0-107, 2.4-116 and 2.5-120 (see table, below). Having four product models with different power ratings and rotor sizes does give the project developer more choice, but if all four products could be sold, and only one model is sold for a given project site, then the return on capital for the other three products is diminished because production volumes on that model are lower.

For many wind turbine OEMs, including those who are already well entrenched, they can enhance shareholder value by focusing on the development of a product portfolio that optimizes return on capital as much as it optimizes LCOE.

Next steps on product portfolio development by larger OEMs as well as up and coming OEMs in the US market such as Nordex / Acciona, Senvion and Goldwind will have a profound impact on the future growth and profitability.

Wind Watch

Wind Watch is published every Monday, Thursday and Friday.

Until then, please have a look at one of our latest member Q&As, in which Frances Salter spoke to Peter Bachmann of Scottish Equity Partners. Here's an excerpt and you can read the full piece by clicking on the link below.

Member Q&A: Peter Bachmann,

Scottish Equity Partners

By Frances Salter

Of the deals you’ve worked on, which is your favourite and why?

That’s a wind farm which we developed in the Republic of Ireland that got energised just before Christmas last year, called Curraghderrig Windfarm - named after the area which it sits on the north-west coast of Ireland.

The reason it was probably my favourite deal was that it combined all the things I really enjoy. It involved building a relationship with a developer in the Republic of Ireland, and the discussion started off looking quite openly at opportunities. Then this particular project came up: they’d described it as shovel-ready in October/November 2016, then it took us until June 2017 to get to financial close.

We had to do a lot of work to get the contractual suite in shape, and had to enter into lots of negotiations with residents about noise mitigation and other things to facilitate the project. It also involved securing project finance from the Bank of Ireland which was an in-depth process and not as advanced as we had been told.

At a deal level it involved a back-to-back special purchase agreements with the original developers, who were then selling the project to Rengen, who were then selling the project to us. So it was quite a complicated structure. It required a lot of heavy lifting on a wide range of issues, but ultimately it was successful and came to a financial close, and then recently to an operational phase, so that was really pleasing.

When we went to the site for the first time to see the turbines...

A Word About Wind spoke to Steve Lockard, CEO of TPI Composites and incoming chair of the American Wind Energy Association, in our Finance Quarterly report that came out earlier this month. Here are three of the key points.

A Word About Wind spoke to Steve Lockard, CEO of TPI Composites and incoming chair of the American Wind Energy Association, in our Finance Quarterly report that came out earlier this month. Here are three of the key points.

.png)

In our most recent Finance Quarterly report, we’ve taken an in-depth look at one of the world’s fastest-growing and most dynamic wind markets: North America.

In this report, we also spoke to some of the industry’s top figures – including Steve Lockard, CEO at TPI Composites and incoming chair of the American Wind Energy Association. If you’ve not yet had a chance to read the report, you can do so here. In the meantime, here are three take-home points from our conversation with Steve:

- 1. It’s economics, rather than policy, that will drive forward expansion in the wind market in North America and overseas.

“The one thing we are learning is that low cost wins,” Steve said. “When the economics are good, the policy stuff is easier. When we’re too expensive and reliant on policy, then we end up with boom and bust cycles.”

The key factor in driving down costs is the development of new technologies: “Towers are getting taller, rotors are getting larger … Every time we invest in bigger blades, the cost of energy comes down and the business gets better, fundamentally. The economics of wind get better.”

As a result, the wind sector can become less reliant on government policy, as more major coal players cashing see the appeal of wind farms: “Even if our president withdraws from the Paris agreement, the utilities are embracing de-carbonising,” he said.

2. Transmission is the next big challenge – but there’s no shortage of investors.

Wind developers in the US are currently facing the challenge of how to transmit electricity from the areas with the most wind farms to the cities with the most electricity. But happily, investors are very interested in electricity lines.

While Steve professed not to be an expert in transmission, he said: “There are plenty of investment dollars for conservative physical assets with long- term contracts, but that’s not the risky or hard part... It’s more about where is it windy, where is the load needed, and how many jurisdictions do you go through to get from here to there.”

It’s too early to tell whether Trump’s infrastructure plan will help the problem of transmission, but there are reasons to be optimistic.

3. TPI has ambitious overseas growth plans too.

Steve explained that the growth rate in emerging markets such as Mexico, Turkey and India would make them a significant driver of TPI’s growth over the next five years: growth rates in these countries are predicted to be around 9% annually, compared to 0.8% annual growth in the more mature markets.

“You can imagine we’d be building plants where the growth rates are higher,” he added. The company has plans to expand outside of the wind business too: they are currently diversifying into the development of electric vehicles.

You can hear more from Steve Lockard and a host of other North American wind industry experts at our Financing Wind New York conference on 30th May.

No region is off-limits. In the last 12 months, we’ve seen global infrastructure managers Brookfield, Global Infrastructure Partners and Macquarie conclude a series of big renewables deals around the world. Wind now attracts players with deep pockets.

And that means large institutions can’t confine their investment horizons to Europe and North America. Many are equally comfortable investing in renewable energy in the Asia-Pacific region too. This is now a key market for firms looking to diversify.

The importance of Asia-Pacific in global wind is hardly a revelation. In January, consultancy PwC reported that, in 2016, the renewable energy sector in Asia-Pacific countries attracted $115bn of $242bn invested globally in renewables. Almost half of that amount was invested in the wind sector. That includes the huge amount of investment in building new wind farms in China, for example.

That may not be earth-shattering, but it does give context to some of the deals concluded in the region this year.

For example, Canada Pension Plan Investment Board has so far invested $66.6bn in all sectors in Asia-Pacific. That ominous-looking figure includes its recent $247m investment to support Indian developer ReNew Power’s acquisition of Ostro Energy.

We see parallels with another deal concluded last quarter, when US investment fund Global Infrastructure Partners completed the acquisition of Singapore-based developer Equis Energy for $5bn. This is set to provide GIP with a platform to expand in the Asia-Pacific region, including Australia, India, Indonesia and Japan.

Likewise, Australia’s Macquarie Infrastructure & Real Assets this month achieved a $3.3bn close of its second Asian infrastructure fund, which is set to target deals in the Asia-Pacific region in infrastructure, storage and renewables including wind.

So why are multinational renewables investors looking at the Asia-Pacific region now?

The first and most obvious reason is diversification. More mature markets including Germany, the UK and the US are now facing political uncertainty, end of subsidies and rising interest rates. Yes, they are still established markets and that may offer a degree of security, but it also means lower returns, and so investors are looking into other promising countries to diversify their portfolio.

Second, investing in Asia-Pacific makes sense from an economic perspective. Over the last 15 years, the region has seen its share of world GDP grow from just 7% to over 20% at the expense of developed markets. Its abundant natural resources and the increasing value of its industries have contributed to this growth.

And third, countries in the Asia-Pacific region are forecast to account for around 60% of global energy use between now and 2040. Since the costs of implementing and maintaining renewable energy assets have kept falling down in the past few years, many governments in the region are now committing to accelerate the transition to sustainable energy by focusing on renewables, wind and solar in particular.

Investing in the region still comes with risks, though.

For example, the World Economic Forum lists economic risks, cybersecurity, socio-political instability and uncertain prospects for international trade due to an increase in protectionist measures among the challenges that investors of every sectors have to face in the region.

Meanwhile, PwC lists restrictions on foreign investment and high levels of corruption among the challenges for renewable investors.

For investors, this means they need to use extra caution when approaching these markets, even when governments are trying to attract them. Many politicians in the region have implemented favourable regulatory and legal frameworks for renewable energy; and some of them, including Japan, India, Thailand and South Korea, are planning some form of competitive selection process for renewables, including wind farms.

This means there is no shortage of opportunities for investors, who often decide to diversify their exposure across different countries within the Asia-Pacific region so that they can avoid being exposed to the risks of a single country. With the rise of deep-pocketed global wind investors, such strategies could be key.

What has 16 law firms, eight finance firms, and no energy firms?

And no, it’s not a joke. Lesbian, gay, bisexual and trans charity Stonewall published its annual report of the top 100 employers in the UK for supporting LGBT employees in February. This includes a host of names familiar in energy – Bank of America Merrill Lynch, Macquarie, Pinsent Masons and so on – but no energy firms.

Why is this the case? That’s a tough one to answer. Stonewall told me it doesn’t like to single out particular companies or sectors as needing improvement. What we know is that 434 companies with 3.9million employees took part in the research, but we don’t know for sure if energy firms didn’t apply, or did but fell short of the 100.

Either way, it tells us there’s room for improvement in the energy sector, and it’s in the interests of businesses to take this seriously. A sector can only be as good as the people it attracts, and so there must be an interest in this industry – including wind – in taking the steps needed to attract and retain the best people. Taking more steps to support LGBT people at work will only help with that.

And it’s not a small issue. We estimate there are around 72,000 LGBT people working in wind globally.

An annual review of jobs from the International Renewable Energy Agency in 2017 said there are 1.2million people working in the wind industry globally; and, if we look at recent studies, we see that 6% of Europeans identify as LGBT. If we combine these figures, we can get a sense of the size of this issue.

Likewise, US figures showed 0.3% identified as transgender, which would be 3,600 people working in wind. We can’t be sure on the numbers but that's not the point. The point is we can't ignore them.

And there's the anecdotal evidence too. I’ve been writing about the wind industry for four years and I’ve spoken to hundreds of people, but I find it surprising that I haven’t yet met anyone who feels happy to say, even in passing, they’re anything other than straight. Maybe I don’t make people feel comfortable enough to share that. Maybe we’d rather be talking about new wind turbines. But I look forward to the day when people feel happy to talk about their partner just like I talk about my wife and kids, if they want to do so.

Of course, that’s easy to say. The reality is more complicated.

We get some useful background from a Stonewall presentation at an inclusion and diversity event run by Energy UK last month. This identified that 24% people who work in energy had experienced negative comments or conduct from their colleagues about their sexuality, compared to 18% in all businesses. This also showed that firms in the energy sector have fewer visible LGBT role models than in other industries although, in wind, a LGBTQ networking event at next month's AWEA Windpower conference might help.

So what can companies do? Well, while Stonewall doesn’t like to single out energy in its top 100, it does share some useful figures on what the 434 companies that took part are doing to support LGBT employees. This could help to inspire others:

- 79% said they had an LGBT employee network group

- 73% use social media to support on LGBT issues

- 65% worked with other organisations on LGBT equality

- 46% supported employees to become visible role models

- 43% had discussed LGBT equality with senior managers

You can look here for ideas more ideas along these lines. It’s also worth noting that the Energy UK event included insights from firms such as EDF, Innogy, Orsted and RWE about what they’re doing on equality and diversity generally. I hope in the coming years we get to see wind companies having an impact on the top 100. We may think of wind as progressive, but there’s much to be done.

Wind Watch

Out now: 20 Predictions for Wind in North America

By Richard Heap

I've been told everyone has a book in them. For us, it's an e-book.

Yes, earlier this month, the team at A Word About Wind have put out our first e-book, '20 Predictions for Wind in North America'. This is ahead of two major conferences in the US next month: our ownFinancing Wind New York on 30th May, and AWEA Windpower.

This free report gives our views on the 20 big trends we expect to shape the wind industry in the US and Canada by the end of 2019.

This includes a look at tax reforms; changes in the power purchase agreements market; consolidation among the major turbine makers; transmission; cybersecurity; and more. If you want a quick round-up of big industry talking points ahead of those events, this is for you.

And yes, some of the predictions may look familiar to some of our regular readers, but we've made sure to bring it up-to-date with the latest industry data and new ideas on North American wind. If this sounds like your sort of thing, you can get a copy here.

Wind Watch

Wind Watch is published every Monday, Thursday and Friday.

Until then, please have a look at one of our latest blog posts, on whether offshore wind investors can trust the Polish government. Here's an excerpt and you can read the full piece at the link below:

Why should offshore wind investors trust the Polish government?

By Ilaria Valtimora

Only 51MW of wind capacity was installed in Poland last year. That number comes from the International Renewable Energy Agency’s Capacity Statistics Report, which was published last week.

It also comes as no surprise. The Polish government, led by the Law & Justice Party since 2015, has pursued a set of anti-wind policies in the last three years to prioritise growth in coal. But this may be about to change as the country looks set to become one of the most promising emerging markets for offshore wind in Europe.

This year we have seen a series of promising signs.

In January, Polish think tank the Foundation for Sustainable Energy said that the country could install 4GW of offshore wind capacity in the Baltic Sea by the end of 2030 and 8GW by the end of 2035. It has also committed to the Memorandum of the Polish Offshore Energy Sector, which has been signed by 44 entities...

Continuing in our series of member Q&As, we spoke to Peter Bachmann of Scottish Equity Partners. If you'd like to take part, email us at editorial@awordaboutwind.com

Continuing in our series of member Q&As, we spoke to Peter Bachmann of Scottish Equity Partners. Peter is an investor with over £1bn equity deployed in over 100 successful global infra investments, covering all sectors from social to economic to energy. He is currently a Director at Scottish Equity Partners (£1.1bn FUM) where he is leading new investment activities for the £135m Environmental Capital Fund (ECF). ECF is investing in low-carbon focussed projects and companies across all energy sectors. If you'd like to take part in a member Q&A, email us at editorial@awordaboutwind.com.

Of the deals you’ve worked on, which is your favourite and why?

That’s a wind farm which we developed in the Republic of Ireland that got energised just before Christmas last year, called Curraghderrig Windfarm - named after the area which it sits on the north-west coast of Ireland. The reason it was probably my favourite deal was that it combined all the things I really enjoy. It involved building a relationship with a developer in the Republic of Ireland, and the discussion started off looking quite openly at opportunities. Then this particular project came up: they’d described it as shovel-ready in October/November 2016, then it took us until June 2017 to get to financial close.

We had to do a lot of work to get the contractual suite in shape, and had to enter into lots of negotiations with residents about noise mitigation and other things to facilitate the project. It also involved securing project finance from the Bank of Ireland which was an in-depth process and not as advanced as we had been told. At a deal level it involved a back-to-back special purchase agreements with the original developers, who were then selling the project to Rengen, who were then selling the project to us. So it was quite a complicated structure. It required a lot of heavy lifting on a wide range of issues, but ultimately it was successful and came to a financial close, and then recently to an operational phase, so that was really pleasing.

When we went to the site for the first time to see the turbines spinning, it was amazing, it was a really nice project. It’s relatively small as it’s just a 4.6MW project, but sometimes small projects take more work and are harder to get over the line as you don’t have the same budget as when you’re working on a bigger project.

Which trends will affect the wind sector most in the next 5-10 years?

We’re going to see a continued fall in the price of wind energy, as I think technology is going to continue to improve. Cost reduction also then creates many more viable projects. More generally, the trend we’re seeing is that renewables are becoming a lot more accepted again. There was a period where renewables appeared to be the dark sheep of the energy world but now people are realising they can be cost-effective, so hopefully they will become a bigger part of the mix. We need to do everything we can to make sure people accurately understand the true cost of fossil fuels in generation, and properly incentivise renewable generation.

What are the most important lessons you’ve learned during your career?

I suppose a few things. With regards to working with other parties, you really have to work with people who want to work with you: the most difficult situations we’ve found ourselves in have been when we’ve entered into a project where the partner is saying that they could do it themselves. You need to work with people who recognise the benefits that you can bring.

To me it’s really about how important relationships are. This industry is incredibly small and your relationships and your reputation within that are the most important things that you’ve got, so you must do whatever you can to ensure that you behave professionally and ultimately the way you’d want to be treated yourself.

Do you have a mentor and what did they teach you?

I haven’t had a direct mentor as such, but I’ve been lucky enough to work with people who I’ve picked up various things from. I’ve worked with a range of managers and tried to pick up their good traits. The main thing that I’ve learned from them is the value of relationships.

What are some of the biggest challenges facing the wind industry?

The big challenge is to try to get the wider market to recognise the true cost of carbon in other forms of (non-renewable) generation. If we can really get that cost properly reflected, then there’s a strong chance we can change the generation mix from carbon based to renewables. The low cost of carbon is strongly linked to the fact that industries like oil and gas get lots of subsidies, many of which are not transparent to the public.

Another big challenge in the post-subsidy renewables world is the cannibalisation of renewables on themselves: when you have costs coming down every year, you get to a point as an investor where you say actually, is it worth investing today, because if I wait until tomorrow I might have a more efficient turbine or a lower price. That can then put you in a self-fulfilling spiral where you stall any new investment.

The final challenge is ensuring that planning authorities, grid operators and government have a joined- up approach in encouraging wind.

The French government has been looking at how to turn the UK’s impending exit from the European Union to its advantage. Those dastardly French! Coming here and using perfectly fair methods (i.e. adverts on the London Underground) to tempt firms away.

But, sarcasm aside, there are sectors where the UK is conspiring to cede its early-mover advantage to France. One is floating wind.

We know that the UK currently hosts the largest operational floating wind farm – the 30MW Hywind Scotland – but political headwinds look set to make any subsequent schemes far tougher to deliver. This could hand the advantage to firms in France.

No doubt this will be a talking point at the floating wind-focused FOWT 2018 event in Marseille this month. There are plenty of steps needed to commercialise floating turbines, and whoever is able to take them first will be in a strong position to become an early leader in a market that could transform offshore wind.

Industry sources have suggested that the cost of floating offshore wind could fall to €40-€60/MWh by 2030, and this is likely to be sooner given this industry’s record on driving down costs. This could open up huge parts of the ocean for offshore wind – but only if companies can work to make the industry make financial sense.

The UK has emerged as an early leader, and for good reason. Statoil and Masdar completed Hywind Scotland in October 2017; and the country is also home to the world’s largest offshore wind market. But this is under threat from the government.

We only need to look back to February to see why. That is when RenewableUK and a group of floating wind specialists lobbied the UK government to extend the Renewable Obligation Certificate subsidy scheme to support the three floating projects planned in UK waters. Yes, it would be different to the way other sectors are being treated, but it could help establish the UK in this potentially huge industry. A great post-Brexit story, right?

No deal, said UK energy minister Claire Perry. She said ROCs wouldn’t be extended as it has been clear for years when the scheme would end, and could also open up the government to legal challenges. It could be disastrous for two or three projects.

For example, 2-B Energy and Hexicon have said that their Forthwind and Dounreay Tri schemes – with total capacity of up-to-60MW and 10MW respectively – would not be able to proceed without ROC support.

The third, where work could start in time to win support, is the 50MW Kincardine by Pilot Offshore Resources and ACS Cobra Wind. That would leave the UK with a 'pipeline' of one project.

That could hand the initiative to other countries that are looking at floating offshore wind farms, such as France, Japan and the US. For now, we think France is best-placed.

We saw this month that plans are afoot for a 100MW-150MW floating scheme off the coast of California, but US offshore wind is in its infancy. And Japan has a big interest in developing floating technology, but it hasn’t made any major strides since the third turbine was installed at its Fukushima Forward project in 2016.

There is also the 25MW WindFloat Atlantic scheme planned in the waters off the coast of Portugal, but it’s only one project and so won’t help to sustain an industry.

This leaves France well-placed. There are four floating projects totalling 100MW planned in its waters: SBM’s 24MW Provence Grand Large; Engie, EDP and CDC; 24MW Leucate; a Quadran-led consortium’s 25MW Gruissan; and Eolfi and CGN’s 24MW Groix. This could even become the dominant French offshore sector with ongoing uncertainty over fixed-bottom schemes.

Those working in floating wind are urging the government to back up this potential with targets. FEE has a goal for 6GW of floating wind in French waters by 2030 and has urged the government to pursue that with a 2GW tender. Perhaps this is time for France to ignore the tortuous system that is causing high prices in onshore wind and low certainty in offshore wind. We can hope.

Either way, France has a chance to nab an industry from under the UK’s noses. It just needs the confidence to actually do so.

Ahead of the Taiwan Offshore Wind Summit on May 15th-16th, we've taken a look at how state-backed finance could help facilitate the growing Taiwanese offshore wind market.

For the Taiwan Offshore Wind Summit in March 2018, we took a look at how state-backed finance could help facilitate the growing Taiwanese offshore wind market.

March 2018 was a busy month in Taiwan’s burgeoning offshore wind sector – or, at least, that’s how the manufacturers made it look. They’re rarely shy about self-promotion.

MHI Vestas picked up orders totalling 1.5GW from Copenhagen Infrastructure Partners and China Steel last month; and Siemens Gamesa won a 120MW order for the second phase of Swancor’s landmark Formosa 1. That shows that the market is moving.

And it wasn’t just turbine orders: we saw Marubeni and Taiwan Green Power link up to develop a $3bn 600MW scheme. In total, there are offshore wind projects totalling over 10.5GW planned in Taiwan’s waters, and the government has now started its tender to award support for 5.5GW of them, between May and July.

But, in our view, the most interesting deal revealed in Taiwan’s offshore wind sector last month was one with the lowest profile.

New state-backed investments

On 23rd March, the Taipei Times reported that German developer Wpd has secured $2.8bn backing from 12 domestic banks for the offshore projects it is planning in the country: the 700MW Yunlin and 360MW Guanyin schemes. As part of this, it has won funds from two state-backed banks.

Wpd Taiwan chairwoman Yuni Wang announced the funding package at an offshore wind workshop, and it gives a strong indication that there will be state-backed money to support the commercialisation of offshore wind farms in Taiwanese waters. It is a good sign at a time when some investors have questioned the government’s approach.

For example, we wrote in February 2018 that Taiwan’s leaders needed to give developers confidence over the long-term stability of the power purchase agreements it is set to award over the next few months. And the government’s Ministry of Economic Affairs has also been criticised for being too passive, and not doing enough to reduce risks that would deter overseas investors – although this appears less of an issue now.

Wpd said it attracted interest from 39 investors, including 12 local banks and 15 overseas institutions, and secured funding from the likes of Cathay United, CTBC and E.Sun. This investor interest follows big moves in the sector by established offshore wind players including CIP, Macquarie, Northland Power, Ørsted and Wpd. Interest from both industrial and financial players gives us confidence in the sector’s long-term prospects.

But these investors still need government guarantees if they are to build a stable supply chain, and bring the cost of offshore wind down to the levels we are seeing in Europe. The presence of these unnamed state banks could provide the same state-backed support as the UK Green Investment Bank did in Europe.

The problems of securing state-backed investment

And getting these banks to invest is no small feat. Wpd said state-backed investors in Taiwan have been nervous about getting into the fledgling offshore wind sector as a result of a high-profile loan fraud involving Ching Fu Shipbuilding. In February, the Kaohsiung District Prosecutors’ Office charged four Ching Fu executives and one consultant over fraudulent loans they took out after winning a government contract.

Now, if you don’t recognise the name Ching Fu or the case, then that’s no surprise. The case didn’t relate to offshore wind, and Ching Fu isn’t an established player in the offshore wind sector.

Even so, it has made the banks warier about doing deals in untested sectors, and with offshore firms. Wpd said it was able to help state-backed investors overcome their reticence about offshore wind as it’s been working in Taiwan for over a decade.

There’s still a long way to go before Wpd can wow these investors with completed projects, though. First, it has to be among the winners in a highly-competitive tender process, and then it has to deliver two large projects in a market that is still untested.

But, if it can help entice state-backed investors into offshore wind, then it means they can gain confidence in the sector – and other firms should also be able to benefit.

Each year, we host conferences discussing the biggest issues in North American and European wind. Click below to find out more...

Indian developer ReNew Power last week concluded the biggest deal in the Indian renewable energy market to date. It agreed to acquire Ostro Energy from emerging market investor Actis in the country’s largest renewables M&A transaction, which is reportedly valued at INR100bn (€1.2bn).

This deal will help establish ReNew as India’s largest renewables player: it enables the developer to add Ostro’s 1.1GW renewables portfolio to its own, which is now over 5.6GW, of which 2.2GW is wind farms. This gives ReNew a 9% share of India’s wind market.

And the transaction is the most high-profile in an ongoing wave of consolidation in the Indian renewable energy sector. In the last two years, we’ve seen Tata Power buy Welspun's 1.1GW renewables arm; Greenko acquire the 500MW Indian portfolio of SunEdison; and Greenko is also now looking at a $1bn acquisition of Orange Renewables too. This is set to continue in the next few years.

This consolidation activity is a result of wider changes in India, including falling prices of wind energy and the consequent reduction in profit margins.

For example, in an auction in December, tariffs fell to a record-low of INR2,430/MWh (€30.38/MWh). Lower tariffs have cut returns and forced smaller developers to exit the market. Meanwhile, bigger players, which have been able to attract foreign money, have started a way of consolidations to strengthen their positions. Foreign capital is proving crucial.

The ReNew-Ostro deal in particular shows how foreign investors are contributing to reshape the renewable energy market in India.

ReNew has been able to pursue its consolidation strategy thanks to strong funding from overseas investors. The developer is backed, among others, by Goldman Sachs, Japan’s Jera and Canada Pension Plan Investment Board.

The latter, pension fund CPPIB, backed ReNew for the first time in January as it bought a 6.3% stake in the company from the Asian Development Bank for $144m. It has now invested a further $247m in ReNew to support its acquisition of Ostro.

And ReNew is not CPPIB’s only target in India. The Canadian fund set up an office in the country in 2015 and has so far invested around $3.7bn. Last year, it also allocated a further $1bn for public market investments in the country.

Other investment funds are looking at India too. For example, Canadian investment manager Brookfield’s chief executive Sachin Shah said its acquisition of TerraForm Global provided a platform for further growth in the Indian market and it is now reportedly looking to buy renewables assets in India, including wind farms.

Foreign investment has been key to the development of the Indian renewables market. In total, the renewable energy sector in India attracted investment totalling $11bn last year, according to a report published by the United Nations Environment Programme last week. Of this, $7bn went to solar and $4bn to wind.

However, this was down 20% compared to 2016. The country’s renewables sector needs to attract much more capital, if it is to achieve its ambitious renewables goal. Prime Minister Narendra Modi is planning to reach 175GW of installed renewable energy, including 60GW of wind, by 2022. This would require investments totalling up to $125bn in four years, with is triple its current annual, investment by 2022.

But there are some challenges to overcome.

Foreign investors have been focusing their attention on India because its economics and the support showed to the sector by the government are attractive, if compared to other emerging markets. However, the wind sector also faces challenges including policy uncertainty and falling energy demand.

Government policies and auctions have driven up growth and pushed down prices, but they have also increased risks. For example, aggressive bidding and competition have been forcing to bid without adequate financial buffers, embracing higher risks. This has brought smaller developers with little liquidity to exit the market, while foreign investors have focused their attention on bigger and more reliable players.

Foreign investors are helping to reshape the country’s renewable energy market and the ReNew-Ostro deal is an example of it. The government has now to work hard to attract more overseas investment to really make a difference.

We published our latest Finance Quarterly report this week and, for this issue we’ve taken a closer look at the US market ahead of Financing Wind New York on 30th May. Here are eight highlights.

We published our latest Finance Quarterly report in April 2018 and for this issue we’ve taken a closer look at the US market ahead of Financing Wind New York on 30th May. The report is available for our members to download here. Here are eight highlights:

1. This may be the strongest year to date for wind PPAs.

Our deals database reveals that this has been the strongest quarter for power purchase agreements in nearly five years.

Notably, telecommunications company AT&T has signed two PPAs, with a combined size of 520MW. The largest of the two projects, owned by NextEra, totals 300MW.

As we explored in a recent blog, the US wind industry may be on track for its strongest year yet for PPAs. It’s encouraging to see this trend developing despite political uncertainty and falling wholesale power prices in the US.

2. TPI Composites make the case for building in emerging markets.

We enjoyed speaking to Steve Lockard of TPI Composites for this issue: as well as being CEO at TPI, he is also the incoming chair of the American Wind Energy Association.

We were interested to hear about his firm’s plans to expand outside of the US, due to the higher growth rate that can be found in emerging markets: for example, Mexico, Turkey and India, where growth is predicted to be around 9% annually up until 2026, compared with 0.8% annual growth in more mature markets.

3. Wind power in the US is becoming less partisan.

Steve also talked to us about the growing cross-party support for wind power in the US.

TPI is based in the historically Republican state of Arizona, but Steve says that the age where Republicanism was synonymous with being anti-wind is ending. He explains that given Obama’s outspokenness on wind and solar, some Republican adversaries opposed wind for political reasons, but now embrace it for creating jobs and economic activity.

4. The US needs a self-sufficient offshore wind supply chain.

Stephanie McClellan, who leads the University of Delaware’s Special Initiative on Offshore Wind, talked to us about the conditions needed to support growth of offshore wind in the US. She says there is great potential to develop a supply chain in the US, so that local workers and communities can benefit in the growth of this strategically-significant sector.

5. The New York Green Bank could go national.

We also spoke to the New York Green Bank, which was set up in 2014 to fund renewables projects in the state of New York.

The bank has not previously had a major focus on wind as none of the onshore wind projects planned in New York have been big enough to need NY Green Bank funding. However, the award of support for three new onshore projects totalling 734MW opens up new opportunities for the bank.

The bank’s president, Alfred Griffin, told us that the bank could be looking to expand across the US in the coming years. He argues that, rather than individual states setting up their own green banks, it could be more efficient to have one operating nationally.

6. Impacts of tax reform could be less negative than expected.

David Burton, partner at law firm Mayer Brown, gave us reasons to be optimistic about the impact of recent tax reform:

“The phrase I’ve used is that the wind industry dodged a bullet but was hit on the ricochet. The worst fears in terms of changing the tax credit rules weren’t realised, but there are some changes that are detrimental but not fatal.”

For example, David observed that the reduction of the federal corporate income tax rate means that sponsors of wind projects will, by and large, be able to raise less tax equity.

7. We’ve seen interesting developments in emerging markets.

Our databank shows there have been some exciting developments in offshore wind in emerging markets this quarter. For example, Statoil (now Equinor) made a particularly sizeable M&A deal in Poland, buying a 1,200MW project from Polenergia.

This quarter has also seen a good amount of offshore activity in Taiwan, with Ørsted winning environmental consent for four projects totalling 2.4GW.

8. Lots of M&A deals are happening in the Asia-Pacific region.

Our M&A tracker shows that there is ongoing consolidation of the wind sector in the Asia-Pacific region, especially India. This comes at a tough time for the Indian wind market, which is faced with political uncertainty and record-low prices. Developers are consequently faced with reduced profit margins, and so they see acquisitions as a way of reinforcing their positions. The most significant so far this year has been Renew’s purchase of Actis arm Ostro Energy for €1.2bn.

Wind Watch

Out now: Finance Quarterly - North America special

By Richard Heap

Next month, we are due to host our inaugural Financing Wind New York conference, in association with GCube Insurance Services.

And so, in advance of that, we've decided to take a closer look at the state's plans for offshore and onshore wind. This is part of our second Finance Quarterly report of 2018, which we published on Tuesday and which focuses on the North American market.

If you haven't already looked at this report, it includes:

- Analysis of New York's plans for offshore and onshore wind; and offshore wind in the wider northeast US region

- Interview with TPI Composites CEO Steve Lockard

- Profile of Skyline Renewables

- Quarterly look at corporate M&A

- Project M&A, PPA and offshore in Q4

- Our NEW project finance deals tracker

- Q&A with David Burton from Mayer Brown

Click here to download your copy of Finance Quarterly Q2 2018. And we look forward to seeing you at the conference next month.

Businesses are starting to look seriously at developing offshore wind farms in the waters near Poland – but can investors trust a government that has so effectively damaged the onshore wind sector. Ilaria Valtimora reports

Businesses are starting to look seriously at developing offshore wind farms in the waters near Poland – but can investors trust a government that has so effectively damaged the onshore wind sector? Ilaria Valtimora reports

Only 51MW of wind capacity was installed in Poland last year. That number comes from the International Renewable Energy Agency’s Capacity Statistics Report, which was published last week.

It also comes as no surprise. The Polish government, led by the Law & Justice Party since 2015, has pursued a set of anti-wind policies in the last three years to prioritise growth in coal. But this may be about to change as the country looks set to become one of the most promising emerging markets for offshore wind in Europe.

This year we have seen a series of promising signs.

In January, Polish think tank the Foundation for Sustainable Energy said that the country could install 4GW of offshore wind capacity in the Baltic Sea by the end of 2030 and 8GW by the end of 2035. It has also committed to the Memorandum of the Polish Offshore Energy Sector, which has been signed by 44 entities that are looking to support the development of the offshore wind industry in Poland.

And this week, the Polish state-owned transmission system operator PSE has told Polish newspaper Rzeczpospolita that it will be ready to connect 4GW of offshore wind to the power grid by the end of 2027. PSE president Eryk Kłossowski added that if the government carries out the much-needed network upgrades, it would be also able to double this potential capacity to 8GW.

This activity has started to attract key players in the global offshore wind market.

For example, last month, Norwegian oil giant Equinor – previously Statoil – acquired a 50% interest in the Bałtyk Środkowy 2 and 3 offshore wind schemes, which are set to total 1.2GW, from Polenergia. And Poland’s largest utility PGE last month unveiled a plan to develop up-to-2.5GW of offshore wind capacity in the Baltic Sea by 2030.

We can see why growing the offshore wind industry in Poland makes sense.

Offshore wind could benefit the Polish economy in many different ways, including to support industrialisation, raise tax revenues and jobs throughout the supply chain.

Investing in offshore wind farms with a capacity of 4GW would create sufficient scale to locate a large part of the supply chain locally; and Poland already has companies that have been providing components to offshore wind farms. These include turbine foundations, towers, marine cables and transformer stations, as well as vessels for the construction and servicing of offshore wind turbines. This means that investing in building the offshore wind sector in Poland would directly benefit Polish businesses.

For example, in a report published by consulting firm McKinsey in 2016, the cost of building 1MW of offshore wind capacity in Poland was estimated to be at €4m – but this was a figure based on a WindEurope report in early 2016 and so may well have dropped. Even so, using that figure means that Poland would have to attract at least €16bn of investment to install 4GW of offshore wind by 2030. Government support would be crucial to do that.

But will the Polish government be able to attract investors?

Well, the approach that the Polish government has taken so far with onshore wind is not reassuring. The Law & Justice Party delayed and then cancelled the introduction of a tendering system to support wind; brought in a law that increased the distance wind farms had to be built from homes, ruling out huge areas from new schemes; and brought in higher taxes.

In addition, a clear example of how badly onshore wind firms have been treated in Poland can be found in the case of US developer Invenergy, which launched a legal action against the government last year, claiming $700m of damages because of its approach to the wind sector.

But the government might now take a different approach towards offshore wind given the economic benefits that it could produce. After all, the UK has supported growth in the offshore wind sector while being more obstructive to onshore wind, so there is a precedent for a country favouring one over the other. Not everyone’s like Germany.

WindEurope chief executive Giles Dickson, speaking at DNV GL Hamburg Offshore Wind Conference this week, said there were reasons to be optimistic about the growth of offshore wind market in Poland. He said that, while the government has not been friendly to onshore wind, it has now an economic and industrial policy interest in developing offshore wind projects as they create a lot of jobs.

In fact, the Polish government has recently presented to the parliament an amendment to the country’s Renewable Energies Act to allow for offshore wind auctions, and the first one could happen as soon as next year.

That sounds good, but the Polish government has already demonstrated that it can build and then destroy a promising market in onshore wind. We recommend caution.

Wind Watch

The City That Never Sleeps wakes up to wind

By Richard Heap

Next month, we are due to host our inaugural Financing Wind New Yorkconference. And so, in advance of that, we've decided to take a closer look at the state's plans for offshore and onshore wind.

Yesterday we published our second Finance Quarterly report of 2018, which includes the latest data on all the biggest deals in the wind sector globally; and analysis on the North American market.

This special report includes:

- Analysis of New York's plans for offshore and onshore wind; and offshore wind in the wider northeast US region

- Interview with TPI Composites CEO Steve Lockard

- Profile of Skyline Renewables

- Quarterly look at corporate M&A

- Project M&A, PPA and offshore in Q4

- Our NEW project finance deals tracker

- Q&A with David Burton from Mayer Brown

Click here to download your copy of Finance Quarterly Q2 2018.

%MCEPASTEBIN%

Companies in the wind industry are taking steps to support birds, bats and marine life at their developments, and our new e-book predicts we will hear a lot more about innovations here in the coming years. Here are five recent stories we’ve heard about this vital work.

Companies in the wind industry are taking steps to support birds, bats and marine life at their developments, and our new e-book predicts we will hear a lot more about innovations here in the coming years. Here are five recent stories we’ve heard about this vital work.

Ban cats! It’s the only solution. According to a 2013 study of 10,000 birds that died as a result of human activity, nearly three-quarters (7.252) were killed by people’s pet cats.

The other biggest killers included buildings, non-renewable power projects and vehicles, with agriculture and forestry also among the ignominious top six. And how many of the 10,000 deaths could be attributed to wind turbines? Just one – or less than 0.01%.

And yet, despite that, critics of the wind industry from President Trump downwards single out wind farms for special criticism when it comes to bird deaths. This means that there’s pressure on wind farm owners to demonstrate how they plan to protect these species.

In the run-up to our Financing Wind New York conference on 30th May, A Word About Wind has produced an e-book called ’20 Predictions for Wind in North America’ on the prospects for the sector in 2018 and 2019. You can download a copy of the report here. One of our 20 predictions is that project owners will do a lot more to address the impact of their schemes on wildlife; and will also publicise their efforts to help address the criticisms head on.

But how are wind farm developers seeking to help or protect wildlife at their projects? Here are five cool stories we’ve seen recently…

1. The world’s there for oysters

This month, a group made up of Van Oord, Investri Offshore and Green Giraffe won the race to develop a 19MW offshore project in Dutch waters called Borssele 5. The 19MW project is set to be made up of two 9.5MW MHI Vestas turbines and be operational in 2021.

This project may not be huge, but it is notable as it includes technology designed to help cut the costs of offshore wind energy and improve the sector’s environmental impacts. The part that has really grabbed our attention is that the project is set to include artificial reefs that can help to promote biodiversity in the North Sea – and particularly for oysters.

The Netherlands Enterprise Agency has explained that introducing these reefs in the scour protection at the bottom of the turbines would allow oysters to flourish. It said this would be aided because fishermen would not be able to carry out activities around the turbines, such as trawl fishing, that disturbs the seabed.

It wrote in a press release that oyster beds would be planted to support this process:

The oyster beds will prevent erosion of the sea floor around the wind turbines’ foundations and aid in the recovery of the marine ecosystem in the North Sea. Rocks of various types and dimensions will be placed on the seabed to limit the flow of water over it and the disturbance of its sediment, creating an ideal habitat for oysters. The rocks are enriched with calciferous shell material, which provides a good substrate for the oysters. When the bed is planted, oysters in various stages of their life cycle will be added. They will then reproduce and spread throughout the North Sea. Good news for the oysters (if not for gourmands): these oyster beds will not be harvested. Instead, they will remain on the reef to allow further replenishment of the seabed and development of the ecosystem.

2. Golden opportunity to prevent eagle deaths

Five years ago, Duke Energy Renewables was sentenced in a court in Wyoming and handed a $1m fine for violating the Migratory Bird Treaty Act. This was in relation to the deaths of protected birds, including golden eagles, at two of the company’s wind farms in Wyoming.

The case focused on the discovery of bodies of 14 golden eagles and 149 other protected birds, including hawks and blackbirds, at its Campbell Hill and Top Of The World wind farms in Wyoming. This was the first time the Obama administration took legal action against a wind farm owner over the deaths of protected birds at a wind farm.

However, far from shying away from the problem, Duke Energy Renewables has sought to address it, and in January it announced that it would roll out an artificial intelligence-based defence system at Top Of The World. The idea is to help it detect eagles and prevent them colliding into turbine blades by using system from a firm called IdentiFlight International. It says that the system blends artificial intelligence with high-precision optical technology.

Here’s an explanation of how the technology works from IdentiFlight:

Automatic detection and species determination occur within seconds for birds flying within a one kilometer hemisphere around an IdentiFlight tower. If an eagle's speed and flight path indicate risk of collision, an alert is generated to shut down that specific wind turbine. By providing highly targeted, informed and objective curtailment decisions, unnecessary and costly interruptions are avoided and conservation of protected species is achieved.